The Jeff Wars: Independence vs. Integration in Ad Tech

Kelly Wittmann

September 4, 2025

13

minutes read

The ad tech industry has always thrived on volatility, but this past week underscored just how fragile even the strongest players can be. The Trade Desk, long celebrated as the independent champion of the open internet, saw its stock plummet nearly 40% in a single day. This despite beating Wall Street expectations. What rattled investors wasn’t past performance, but what’s ahead: slower growth, a surprise CFO exit, and the looming shadow of Amazon’s accelerating DSP.

What’s happening isn’t just about The Trade Desk. It’s a window into the future of digital advertising.

For years, an “independent DSP” signaled neutrality and wide-open access to supply. That advantage narrows when integrated platforms—whether Amazon, Google, Meta, or emerging retail media networks—can combine authenticated identity, purchase data, premium video inventory and pricing control in one stack. While Amazon offers one of the clearest examples (its advertising services hit roughly $15.7 billion in Q2 2025, up about 23% year over year), this same pattern is playing out across multiple walled gardens.

The buying center of gravity is shifting toward integrated platforms that combine proprietary inventory with rich first-party data—think YouTube ads with Merchant Center product feeds and audience signals, Meta’s graph plus Shops/CAPI, and Walmart Connect applying shopper data to CTV and shoppable streaming.

By Q4 2024, the Amazon DSP accounted for ~32% of all Amazon ad spend among advertisers in one large dataset, while Google's DV360 maintains similar dominance for YouTube inventory access.

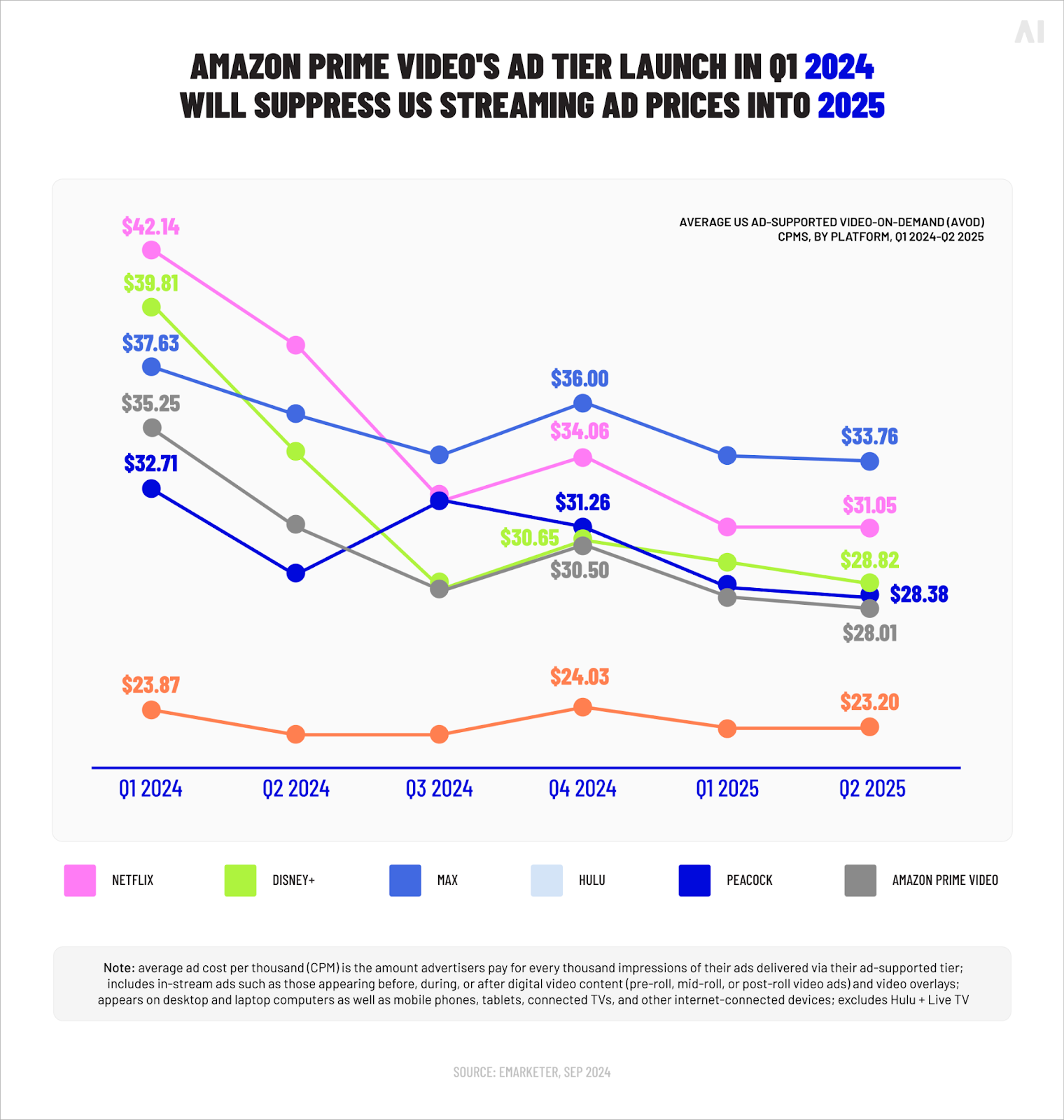

Pic. Amazon Prime Video’s ad tier effect on prices through 2025 (Source).

Price matters too. Multiple agency sources say Amazon has been undercutting rival DSPs on platform fees and offering aggressive commercial terms to win share; some buyers reported tech fees trimmed to around 10% in recent months. When you pair lower fees with access to logged-in audiences and closed-loop retail attribution, independent DSPs face a tougher sell on cost–performance grounds.

Inventory access is tilting as well. Each major platform is increasingly gating premium supply: Amazon with Prime Video ads available via Amazon DSP in both managed-service and self-serve modes; Google with YouTube Select premium lineups; Meta with Reels inventory. And the June 2025 Amazon–Roku deal makes Amazon DSP the exclusive way to reach Roku’s logged-in CTV audience via a shared identifier.

The trend is clear: platforms are scaling ad-supported viewing and tightening access.

Independence still matters for control, transparency and cross-publisher activation, but make diversification the hero: keep an open-internet DSP and at least one platform-native route live, and adjust the mix based on performance, bandwidth and scope rather than ideology.

{{the-jeff-wars-1="/tables"}}

Over-reliance on a single DSP is risky

The Trade Desk’s sharp, ~38% single-day stock drop after its August 2025 earnings and CFO transition was a reminder that even category leaders can stumble. Concentrating spend with any one platform compounds operational and commercial risk—guidance resets, leadership changes or product shifts can quickly ripple into pricing, service levels or roadmap priorities.

There’s also platform continuityrisk you don’t control. In May 2025, Microsoft announced it will shut down Microsoft Invest (formerly Xandr/AppNexus) by early 2026, pivoting toward AI-powered buying tied to its own properties. Buyers dependent on that DSP now face migrations, integration rewires and learning-curve costs, illustrating why vendor concentration can become a single point of failure.

Financial plumbing adds another layer. AdExchanger detailed how extended payment terms and late invoices create a cash-flow gap for DSPs that can strain even well-run platforms. If a DSP is squeezed between slow agency payments and faster obligations to supply partners, service disruptions or retrenchment become more likely. A diversified stack helps insulate campaigns from those shocks.

Exclusivity and identity access also argue against putting all spend in one tool.

Each major platform gates certain inventory. If you're not enabled on multiple platforms, you're structurally boxed out of key audiences. The smart play is maintaining access to multiple inventory sources.

Finally, measurement and control benefit from redundancy. Senior analysts and TV buyers note that different DSPs see different supply, apply different algorithms and expose different reporting, which means a second primary DSP can act as a benchmark and a release valve when inventory, fees or performance shift.

In short: independence on its own is no longer enough, and dependence is a liability. Treat optionality across at least two scaled buying routes as standard risk management.

Budgets are flowing where the data lives

Buyers are concentrating dollars where authenticated audiences and purchase signals are strongest. Amazon is a prominent example, but think of it as one case among many; the broader shift is toward platforms that pair logged-in reach with measurable outcomes. Its latest earnings reinforced faster-than-market momentum and confirmed heavyweight status, not a challenger.

{{the-jeff-wars-2="/tables"}}

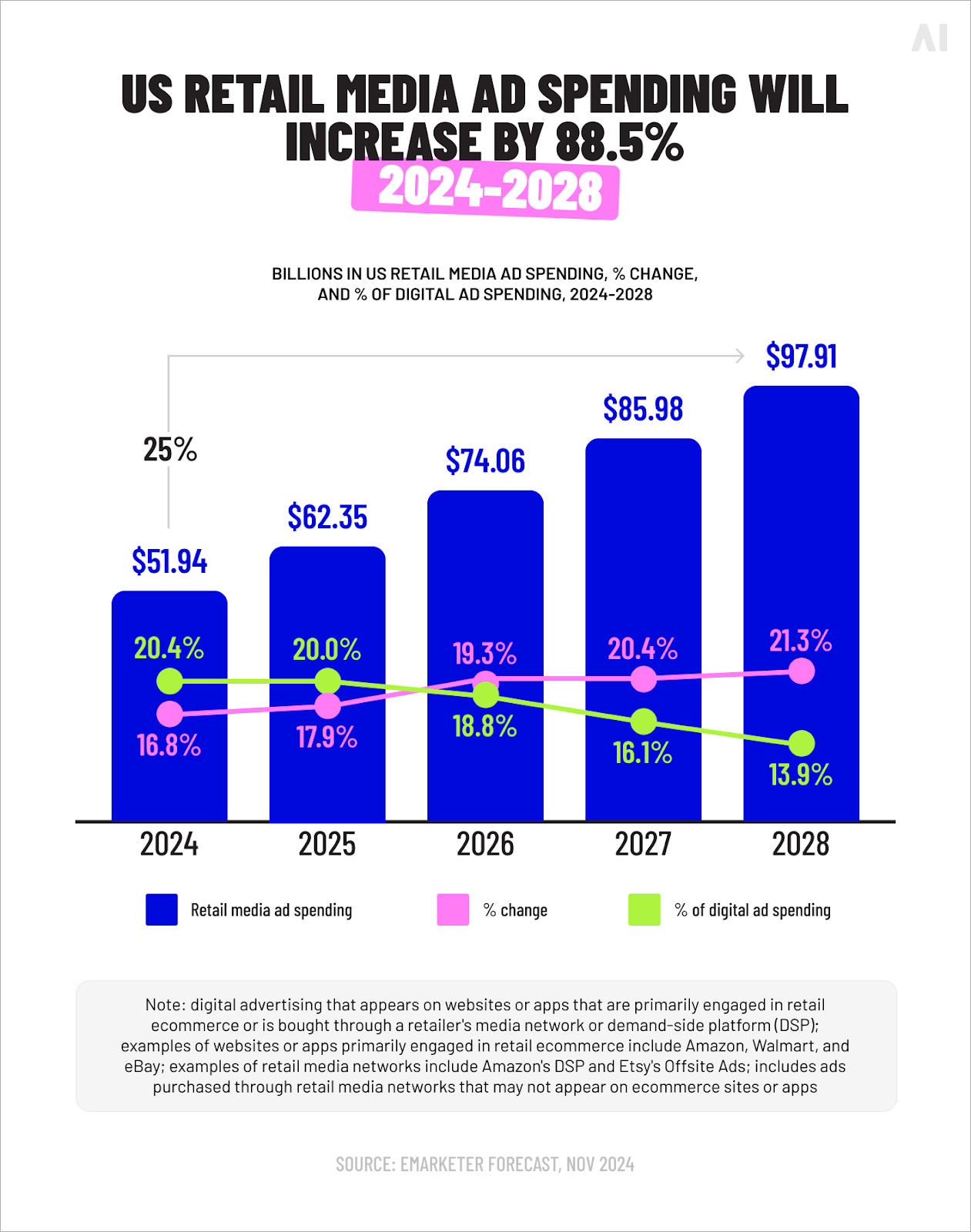

Retail media keeps taking a larger slice of US budgets because it links ad exposure to closed-loop sales. Insider Intelligence/eMarketer expectsUS retail media to top $62 billion in 2025, adding more than $10 billion year over year; other forecasts peg Amazon’s retail-media ad revenues alone at $60+ billion in 2025 and nearly $70 billion in 2026. Importantly, growth isn’t confined to one player: Walmart Connect, Instacart Ads, Kroger Precision Marketing and Roundel are also capturing share as marketers chase authenticated audiences and verified outcomes.

CTV is the other magnet. Insider Intelligence estimatesUS CTV ad spend will reach ~$33.3 billion in 2025 (≈16% YoY), driven by major streamers’ ad tiers. Coming out of the 2025–26 upfronts, several leading streamers (including Amazon) confirmed higher ad loads and new formats, expanding the pool of premium, logged-in inventory available to buyers.

Most of that expansion is paid for by cuts elsewhere. Forecast downgrades and tariff-driven budget cautionare prompting reallocation toward channels that prove performance quickly. Digiday’s interviews with holding-company and independent buyers indicate more clients are shifting incremental spend into platform-native routes (Amazon’s DSP among them) in 2025 to de-risk plans.

Broader market outlooks also point to retail media and performance-oriented channels holding up better than broad social or open-web display when budgets tighten.

The next differentiator: AI + agility

Closed ecosystems are entrenched, so the edge comes from how fast you can plan, activate, and measure across them. The most credible gains right now are in time-to-insight and cross-channel decisioning. For instance, Dentsu reports a 90% reduction in time to media insights after deploying an Azure-based agent that automates data prep and analysis for planners. For mid-sized teams, that speed matters even in a modest pilot—when you’re rebalancing a handful of campaigns across a platform-native route, an open-internet DSP, and direct CTV, rather than rebuilding the whole stack.

Clean rooms are the connective tissue. Amazon expandedAmazon Marketing Cloud this year to allow queries against up to five years of store purchase signals, extending beyond the prior 13-month window. Buyers are using AMC to unify path-to-purchase analysis across retail media and CTV, then piping learnings back into activation. Roku, for its part, evolved its clean-room offering into Roku Data Cloud to expose more granular streaming data via ad-tech and agency APIs—useful for deduplicating reach and frequency when you’re buying both platform-native and open-web CTV.

You don’t need an enterprise build to start; many teams begin with a platform clean room (or lightweight joins) and graduate to broader collaboration as scope and resourcing allow.

Identity standards help you move between walled and open environments without rebuilding everything from scratch. The IAB Tech Lab’s PAIR protocol formalizes privacy-safe match-ups between advertiser and publisher data across the clean-room ecosystem, while UID2 continues to gain adoption among CTV platforms (e.g., LG, Roku partnerships) to improve addressability off-platform. Aim for an interoperable setup that uses what your partners already support, rather than chasing a single ID to solve every use case.

On the platform side, major sellers are pushing more native automation and full-funnel workflows—Amazon within its DSP, and similar automation is advancing across other large streamers and buying tools. Agencies are pairing those native capabilities with parallel learning agendas on a second DSP to benchmark algorithms, verify incrementality, and maintain control over pacing and bid strategies.

Analyst houses agree that AI’s payoff is operational: faster cycles, better targeting from first-party data, and more precise measurement. McKinsey’s latest AI research flags workflow redesign and governance as prerequisites for value capture; Gartner’s 2025 outlook reinforces that marketing leaders should treat AI as a process accelerator embedded in planning and activation, not a silver bullet.

Built this way, even smaller teams can shift spend within days as channels or fees change—without promising enterprise-scale lifts out of the gate.

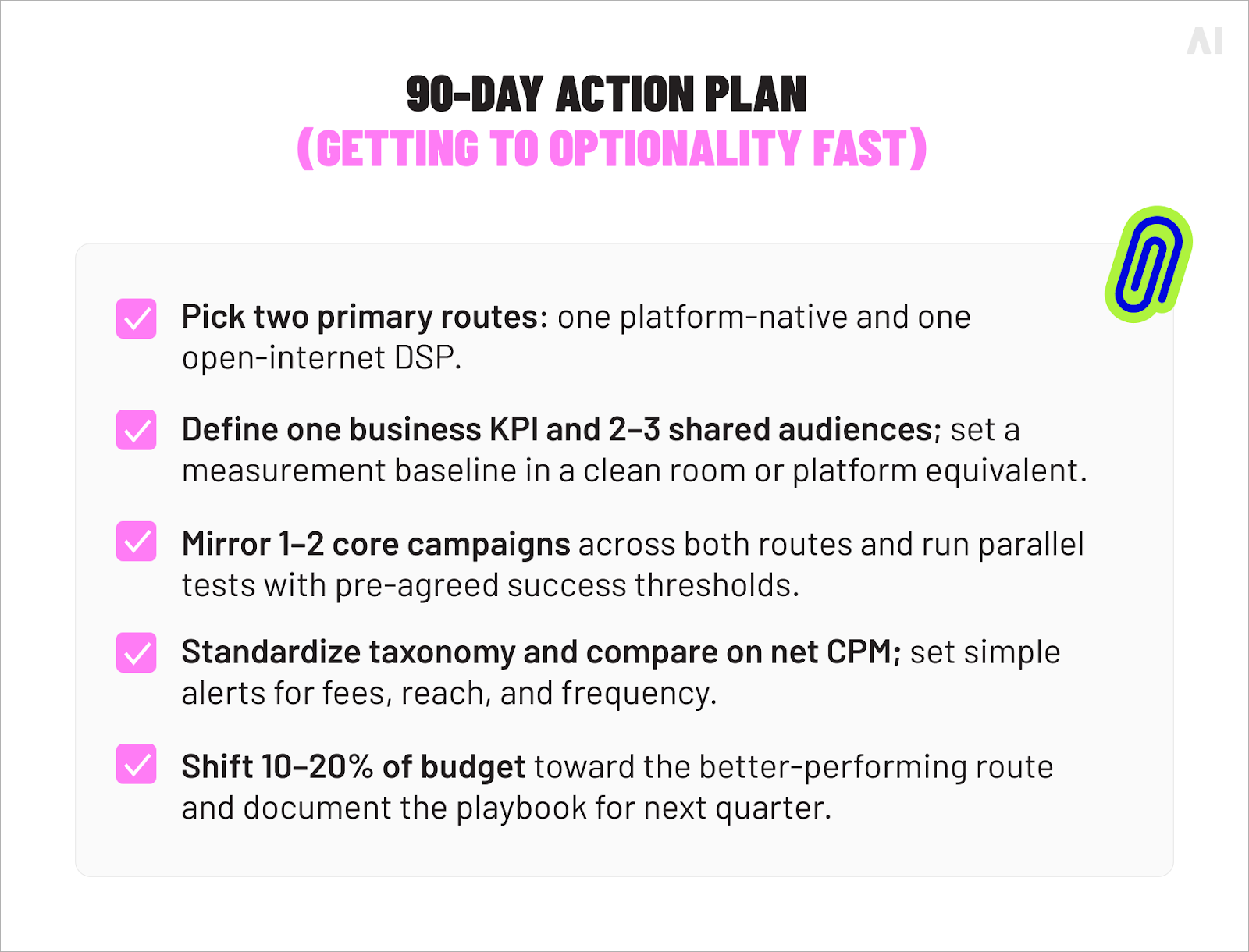

📌 What to do now: set two primary routes, keep the clean room (or a platform equivalent) as your measurement hub, and use the same audiences and a single business KPI across both. Run parallel tests where it fits, let automation shorten the path from signal to decision, and steer budget toward what proves lift. This won’t unwind consolidation, but it will give you the flexibility to work confidently inside and outside the gardens.

Where this leaves agencies and brands

The “Jeff Wars” aren’t really Jeff Green vs. Jeff Bezos; they’re independence vs. integration, optionality vs. consolidation. Agencies caught in the middle will need to decide: double down on a single platform’s promise, or build a multi-DSP strategy that ensures flexibility.

From my perspective, the winners won’t be the ones who pick the “right” DSP, but the ones who refuse to put all their chips on the table of any one provider. Independence alone isn’t enough, but independence combined with open access and the ability to move fluidly across ecosystems is what will keep agencies resilient.

In other words, the future belongs to those who operate with an open garden mindset: neutral, agile, and ready to connect the dots across walled gardens and the open internet alike.

If you’re rethinking your plan, we can help. AI Digital works with brands and agencies to pressure-test their mix, map risk exposure, and stand up a two-DSP baseline. If you’d like a working session to explore the best route for your team, reach outand we’ll chart a practical plan together.

Blind spot

Key issues

Business impact

AI Digital solution

Lack of transparency in AI models

• Platforms own AI models and train on proprietary data • Brands have little visibility into decision-making • "Walled gardens" restrict data access

• Inefficient ad spend • Limited strategic control • Eroded consumer trust • Potential budget mismanagement

Open Garden framework providing: • Complete transparency • DSP-agnostic execution • Cross-platform data & insights

Optimizing ads vs. optimizing impact

• AI excels at short-term metrics but may struggle with brand building • Consumers can detect AI-generated content • Efficiency might come at cost of authenticity

• Short-term gains at expense of brand health • Potential loss of authentic connection • Reduced effectiveness in storytelling

Smart Supply offering: • Human oversight of AI recommendations • Custom KPI alignment beyond clicks • Brand-safe inventory verification

The illusion of personalization

• Segment optimization rebranded as personalization • First-party data infrastructure challenges • Personalization vs. surveillance concerns

• Potential mismatch between promise and reality • Privacy concerns affecting consumer trust • Cost barriers for smaller businesses

Elevate platform features: • Real-time AI + human intelligence • First-party data activation • Ethical personalization strategies

AI-Driven efficiency vs. decision-making

• AI shifting from tool to decision-maker • Black box optimization like Google Performance Max • Human oversight limitations

• Strategic control loss • Difficulty questioning AI outputs • Inability to measure granular impact • Potential brand damage from mistakes

Managed Service with: • Human strategists overseeing AI • Custom KPI optimization • Complete campaign transparency

Fig. 1. Summary of AI blind spots in advertising

Dimension

Walled garden advantage

Walled garden limitation

Strategic impact

Audience access

Massive, engaged user bases

Limited visibility beyond platform

Reach without understanding

Data control

Sophisticated targeting tools

Data remains siloed within platform

Fragmented customer view

Measurement

Detailed in-platform metrics

Inconsistent cross-platform standards

Difficult performance comparison

Intelligence

Platform-specific insights

Limited data portability

Restricted strategic learning

Optimization

Powerful automated tools

Black-box algorithms

Reduced marketer control

Fig. 2. Strategic trade-offs in walled garden advertising.

Core issue

Platform priority

Walled garden limitation

Real-world example

Attribution opacity

Claiming maximum credit for conversions

Limited visibility into true conversion paths

Meta and TikTok's conflicting attribution models after iOS privacy updates

Data restrictions

Maintaining proprietary data control

Inability to combine platform data with other sources

Amazon DSP's limitations on detailed performance data exports

Cross-channel blindspots

Keeping advertisers within ecosystem

Fragmented view of customer journey

YouTube/DV360 campaigns lacking integration with non-Google platforms

Black box algorithms

Optimizing for platform revenue

Reduced control over campaign execution

Self-serve platforms using opaque ML models with little advertiser input

Performance reporting

Presenting platform in best light

Discrepancies between platform-reported and independently measured results

Consistently higher performance metrics in platform reports vs. third-party measurement

Fig. 1. The Walled garden misalignment: Platform interests vs. advertiser needs.

Key dimension

Challenge

Strategic imperative

ROAS volatility

Softer returns across digital channels

Shift from soft KPIs to measurable revenue impact

Media planning

Static plans no longer effective

Develop agile, modular approaches adaptable to changing conditions

Brand/performance

Traditional division dissolving

Create full-funnel strategies balancing long-term equity with short-term conversion

Capability

Key features

Benefits

Performance data

Elevate forecasting tool

• Vertical-specific insights • Historical data from past economic turbulence • "Cascade planning" functionality • Real-time adaptation

• Provides agility to adjust campaign strategy based on performance • Shows which media channels work best to drive efficient and effective performance • Confident budget reallocation • Reduces reaction time to market shifts

• Dataset from 10,000+ campaigns • Cuts response time from weeks to minutes

• Reaches people most likely to buy • Avoids wasted impressions and budgets on poor-performing placements • Context-aligned messaging

• 25+ billion bid requests analyzed daily • 18% improvement in working media efficiency • 26% increase in engagement during recessions

Full-funnel accountability

• Links awareness campaigns to lower funnel outcomes • Tests if ads actually drive new business • Measures brand perception changes • "Ask Elevate" AI Chat Assistant

• Upper-funnel to outcome connection • Sentiment shift tracking • Personalized messaging • Helps balance immediate sales vs. long-term brand building

• Natural language data queries • True business impact measurement

Open Garden approach

• Cross-platform and channel planning • Not locked into specific platforms • Unified cross-platform reach • Shows exactly where money is spent

• Reduces complexity across channels • Performance-based ad placement • Rapid budget reallocation • Eliminates platform-specific commitments and provides platform-based optimization and agility

• Coverage across all inventory sources • Provides full visibility into spending • Avoids the inability to pivot across platform as you’re not in a singular platform

Fig. 1. How AI Digital helps during economic uncertainty.

Trend

What it means for marketers

Supply & demand lines are blurring

Platforms from Google (P-Max) to Microsoft are merging optimization and inventory in one opaque box. Expect more bundled “best available” media where the algorithm, not the trader, decides channel and publisher mix.

Walled gardens get taller

Microsoft’s O&O set now spans Bing, Xbox, Outlook, Edge and LinkedIn, which just launched revenue-sharing video programs to lure creators and ad dollars. (Business Insider)

Retail & commerce media shape strategy

Microsoft’s Curate lets retailers and data owners package first-party segments, an echo of Amazon’s and Walmart’s approaches. Agencies must master seller-defined audiences as well as buyer-side tactics.

AI oversight becomes critical

Closed AI bidding means fewer levers for traders. Independent verification, incrementality testing and commercial guardrails rise in importance.

Fig. 1. Platform trends and their implications.

Metric

Connected TV (CTV)

Linear TV

Video Completion Rate

94.5%

70%

Purchase Rate After Ad

23%

12%

Ad Attention Rate

57% (prefer CTV ads)

54.5%

Viewer Reach (U.S.)

85% of households

228 million viewers

Retail Media Trends 2025

Access Complete consumer behaviour analyses and competitor benchmarks.

Identify and categorize audience groups based on behaviors, preferences, and characteristics

Michaels Stores: Implemented a genAI platform that increased email personalization from 20% to 95%, leading to a 41% boost in SMS click through rates and a 25% increase in engagement.

Estée Lauder: Partnered with Google Cloud to leverage genAI technologies for real-time consumer feedback monitoring and analyzing consumer sentiment across various channels.

High

Medium

Automated ad campaigns

Automate ad creation, placement, and optimization across various platforms

Showmax: Partnered with AI firms toautomate ad creation and testing, reducing production time by 70% while streamlining their quality assurance process.

Headway: Employed AI tools for ad creation and optimization, boosting performance by 40% and reaching 3.3 billion impressions while incorporating AI-generated content in 20% of their paid campaigns.

High

High

Brand sentiment tracking

Monitor and analyze public opinion about a brand across multiple channels in real time

L’Oréal: Analyzed millions of online comments, images, and videos to identify potential product innovation opportunities, effectively tracking brand sentiment and consumer trends.

Kellogg Company: Used AI to scan trending recipes featuring cereal, leveraging this data to launch targeted social campaigns that capitalize on positive brand sentiment and culinary trends.

High

Low

Campaign strategy optimization

Analyze data to predict optimal campaign approaches, channels, and timing

DoorDash: Leveraged Google’s AI-powered Demand Gen tool, which boosted its conversion rate by 15 times and improved cost per action efficiency by 50% compared with previous campaigns.

Kitsch: Employed Meta’s Advantage+ shopping campaigns with AI-powered tools to optimize campaigns, identifying and delivering top-performing ads to high-value consumers.

High

High

Content strategy

Generate content ideas, predict performance, and optimize distribution strategies

JPMorgan Chase: Collaborated with Persado to develop LLMs for marketing copy, achieving up to 450% higher clickthrough rates compared with human-written ads in pilot tests.

Hotel Chocolat: Employed genAI for concept development and production of its Velvetiser TV ad, which earned the highest-ever System1 score for adomestic appliance commercial.

High

High

Personalization strategy development

Create tailored messaging and experiences for consumers at scale

Stitch Fix: Uses genAI to help stylists interpret customer feedback and provide product recommendations, effectively personalizing shopping experiences.

Instacart: Uses genAI to offer customers personalized recipes, mealplanning ideas, and shopping lists based on individual preferences and habits.

Medium

Medium

Share article

Url copied to clipboard

No items found.

Subscribe to our Newsletter

THANK YOU FOR YOUR SUBSCRIPTION

Oops! Something went wrong while submitting the form.

Questions? We have answers

Have other questions?

If you have more questions, contact us so we can help.

.svg)

.svg)