SVOD, AVOD, and TVOD: A Guide to Video on Demand Models

Sarah Moss

October 29, 2025

17

minutes read

Streaming didn’t just change how audiences watch; it created a set of distinct business models that decide who pays, how content is packaged, and where brands show up. This guide breaks down AVOD vs SVOD vs TVOD—what each model means, when to pick AVOD vs SVOD, and how the mix shapes reach, experience, and return.

Marketers are now choosing between subscription access, ad-funded access, and pay-per-title access—often within the same app. That choice affects everything from audience scale and frequency to creative format, measurement, and pricing power.

In the sections that follow, we’ll explain how each model works in plain terms, map the practical pros and cons, and show where they fit across OTT and CTV distribution. We’ll also compare them side by side, outline when hybrids make sense, and preview what’s next for 2026 so you can plan with confidence.

What is VOD (Video on Demand)?

Let’s start with the simplest idea: video on demand (VOD) is any service that lets people choose a title and watch it immediately rather than waiting for a scheduled broadcast. If you can browse a catalogue, press play, pause, rewind, or resume later, you’re using VOD.

How VOD differs from traditional TV

The easiest way to understand VOD is to contrast it with linear TV across three basics: how you watch, how content is packaged, and how it’s delivered:

Control and timing: Linear TV follows a fixed programme schedule; VOD hands control to the viewer to watch what they want, when they want.

Packaging: Linear TV is built around channels; VOD is built around catalogues and titles.

Delivery: Linear typically travels through terrestrial, satellite, or cable distribution; VOD is delivered over IP networks and accessed through apps.

Where OTT and CTV fit

It helps to separate the business model from the delivery path:

OTT (over-the-top) describes how video reaches the viewer—over the public internet, “on top of” broadband, without needing a traditional pay-TV set-top box. OTT can be watched on phones, tablets, laptops, and TVs.

CTV (connected TV) refers to the device—an internet-connected television (smart TV) or a TV connected via a streaming stick or console. CTV is one of the main screens where OTT apps run.

Put another way, VOD is the on-demand experience, while OTT and CTV are the distribution rails and screen that carry that experience into the home.

⚡ VOD is the experience; OTT and CTV are the rails and screen that deliver it.

{{SVOD-AVOD-and-TVOD-SEO-1="/tables"}}

💡 For a deeper primer on the OTT–CTV distinction, see overview: OTT vs CTV.

The three core VOD monetisation models

VOD isn’t a single way to make money; it’s an experience that can be monetised in different ways:

SVOD: access to the catalogue via a recurring subscription.

AVOD: free or lower-priced access supported by advertising.

TVOD: pay-per-title rentals or purchases (electronic sell-through).

You’ll also see adjacent formats such as FAST (free ad-supported streaming TV), which mimics a linear channel grid inside OTT apps, and vMVPDs (virtual multichannel providers) that bundle live channels over the internet. These sit alongside VOD and often live in the same app, but the three models above are the core building blocks for on-demand viewing.

What is SVOD?

Subscription video on demand (SVOD) is the on-demand model where viewers pay a recurring fee for access to a content catalogue, typically with an ad-free experience. Increasingly, many SVOD services also offer an ad-supported subscription tier alongside a premium ad-free tier, which affects pricing, reach, and how campaigns show up for brands.

💡 For a closer look at ad opportunities within SVOD, see the explainer on Netflix advertising.

How SVOD works

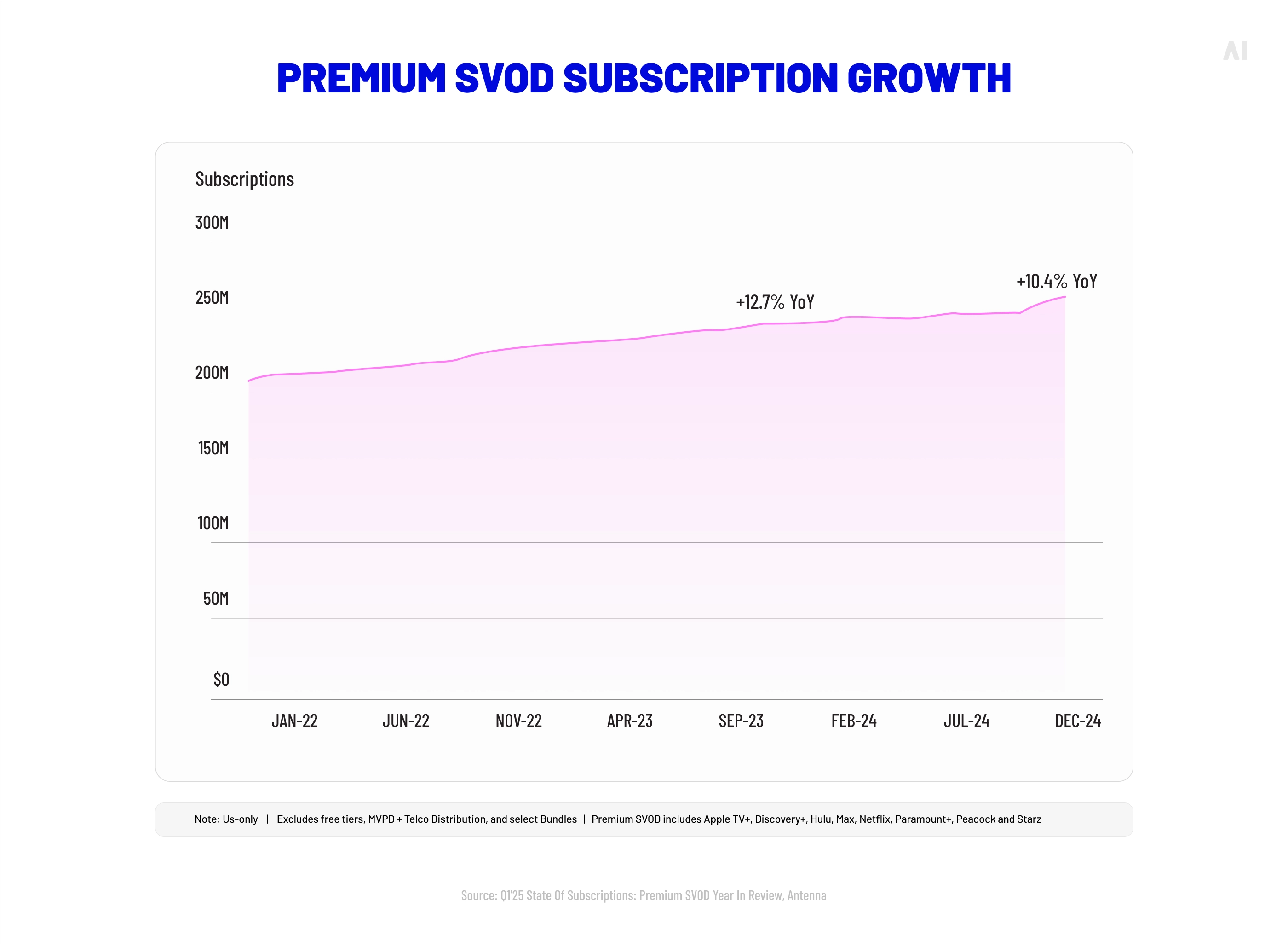

SVOD packages a library of shows, films, and sometimes live events behind a monthly or annual subscription. Users can play, pause, and resume across devices, and billing renews automatically unless cancelled. Many providers now run two SVOD tiers—a lower-priced with ads plan and a higher-priced ad-free plan—so the same service can monetize via both subscription revenue and advertising. In 2024, premium SVOD as a category still grew at double digits, underscoring sustained demand even as platforms reshaped pricing and tiers.

⚡ Two-tier SVOD lets one service monetise with both subscriptions and ads.

The best-known SVOD services include Netflix, Disney+, Amazon Prime Video, Max, and Apple TV+. Several now operate hybrid line-ups with paid ad-supported tiers. Netflix, for instance, reported more than 94 million global monthly active users on its ad-supported plan by May 14, 2025, highlighting how ad tiers have become part of the SVOD toolkit.

⚡ Large ad-tier footprints turn SVOD into premium, addressable TV at scale.

💡 For ad formats and buying routes on Netflix, see the guide to Netflix advertising.

Pros of SVOD

A short list helps clarify where SVOD shines and why marketers should care.

Predictable recurring revenue and stable planning: Subscriptions provide steadier income than one-off transactions, and the premium SVOD category grew about 10.4% in 2024, signaling resilience as services refine pricing and tiers.

Premium viewer experience: Ad-free environments reduce interruption, while ad-supported tiers can extend reach at lower price points—useful for audience scale and frequency planning. Netflix’s large ad-tier footprint illustrates the reach upside for advertisers inside an SVOD service.

Pricing power and packaging: Platforms adjusted prices in 2024–2025, with average ad-free SVOD pricing rising (approx. $11 → $14) and ad-supported plans (~$6 → $7.50), creating clearer value ladders between tiers and more ways to match price sensitivity to content appetite.

Device and distribution breadth: SVOD lives across OTT apps and connected TVs (CTV), benefiting from the broader OTT growth outlook through 2029.

SVOD also carries real trade-offs for both platforms and marketers.

Churn sensitivity: As line-ups and prices change, customers rotate in and out. Antenna’s 2024 figures show monthly churn averaging just under 3% for the year (with quarter-end peaks around 5%), reminding teams to budget for re-acquisition and win-back.

Price pressure and value perception: Broad price rises across the category in 2024–2025 pushed more users toward ad-supported options and selective stacking; U.S. premium SVOD grew, but services also saw periods of contraction and mix shifts as households trimmed ad-free plans.

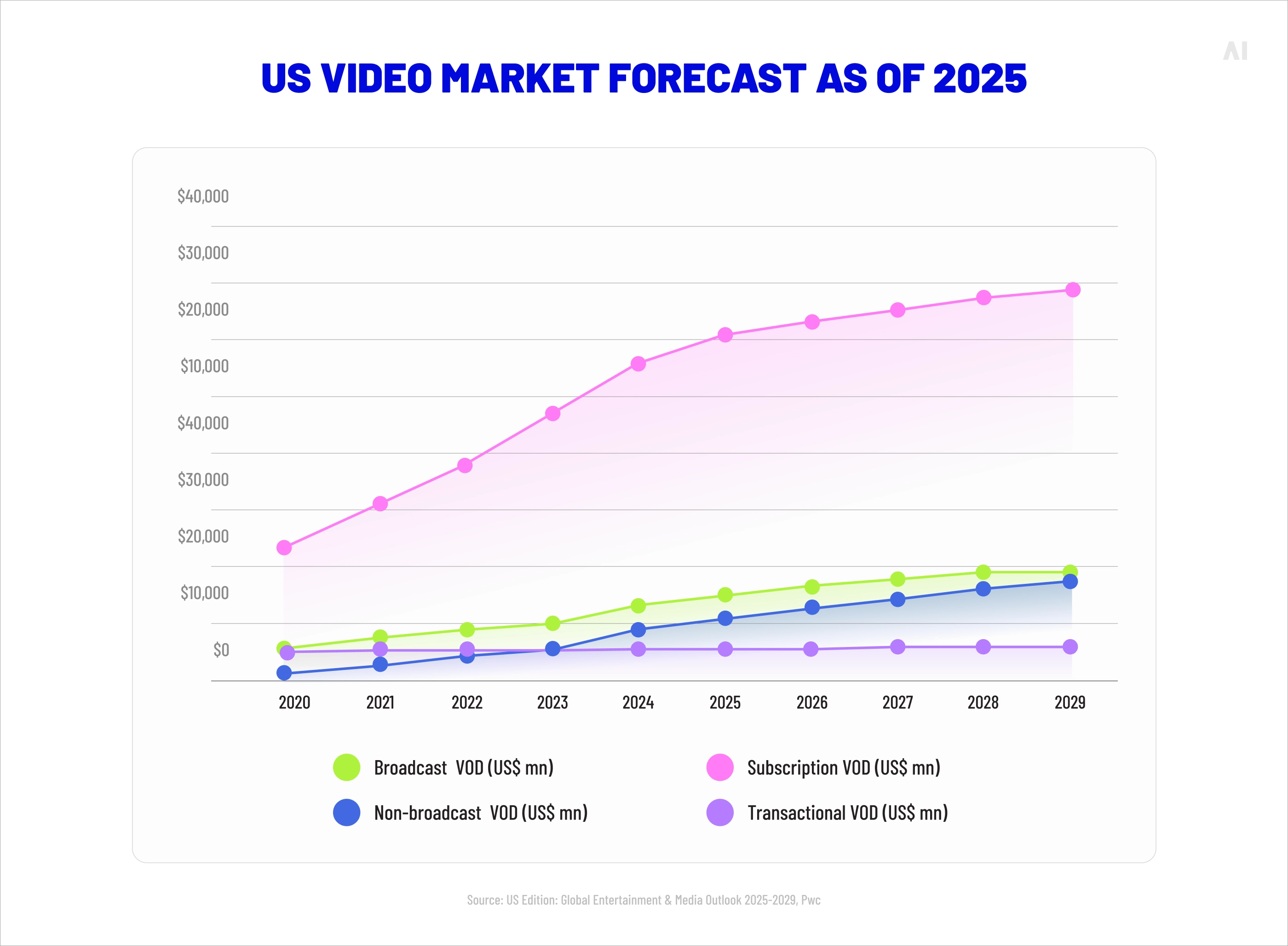

Content cost and fragmentation: Competing for hits is expensive, and catalogues are spread across many apps. PwC’s outlook shows OTT consumer spending overtaking pay-TV by 2027, but profitability still hinges on balancing content spend with tier mix and advertising yield.

Global TV subscription revenue vs global OTT (SVOD & TVOD) revenue

📌 If you’re planning media, the takeaway is straightforward: SVOD now operates on a tiered subscription continuum. The ad-free tier offers premium, interruption-light environments suited to brand storytelling and retention KPIs, while the with-ads tier supplies incremental reach and price efficiency—both inside the same service.

What is AVOD?

Advertising video on demand (AVOD) lets viewers watch on-demand content either free or at a discounted price in exchange for seeing ads. Think of it as the on-demand version of commercial TV: the catalogue is available any time, but playback includes ad breaks the platform sells to brands.

⚡ AVOD trades price for attention—the viewer’s ‘payment’ is time spent with ads.

💡 For a quick primer on how AVOD sits inside broader streaming TV buying, see the guide to streaming TV advertising.

How AVOD works

Before the first frame plays, the service decides what ads to show, how often to show them, and to whom. Most platforms use dynamic ad insertion (DAI) to stitch ads into the stream in real time, typically as pre-roll, mid-roll, and post-roll pods; delivery can be server-side (SSAI) for smoother playback on CTV or client-side in apps and browsers.

⚡ Server-side ad insertion keeps streams smooth on CTV while stitching ads in real time.

{{SVOD-AVOD-and-TVOD-SEO-3="/tables"}}

Audience targeting comes from first-party account data, device signals, contextual metadata, and data-partner segments; buying can be direct, private marketplace, or open programmatic, with brand-safety and measurement layers on top.

AVOD inventory spans mobile, desktop, and connected TVs (CTV), where streaming now commands a large share of TV time and where ad-supported streaming has been gaining the most share. Nielsen+1

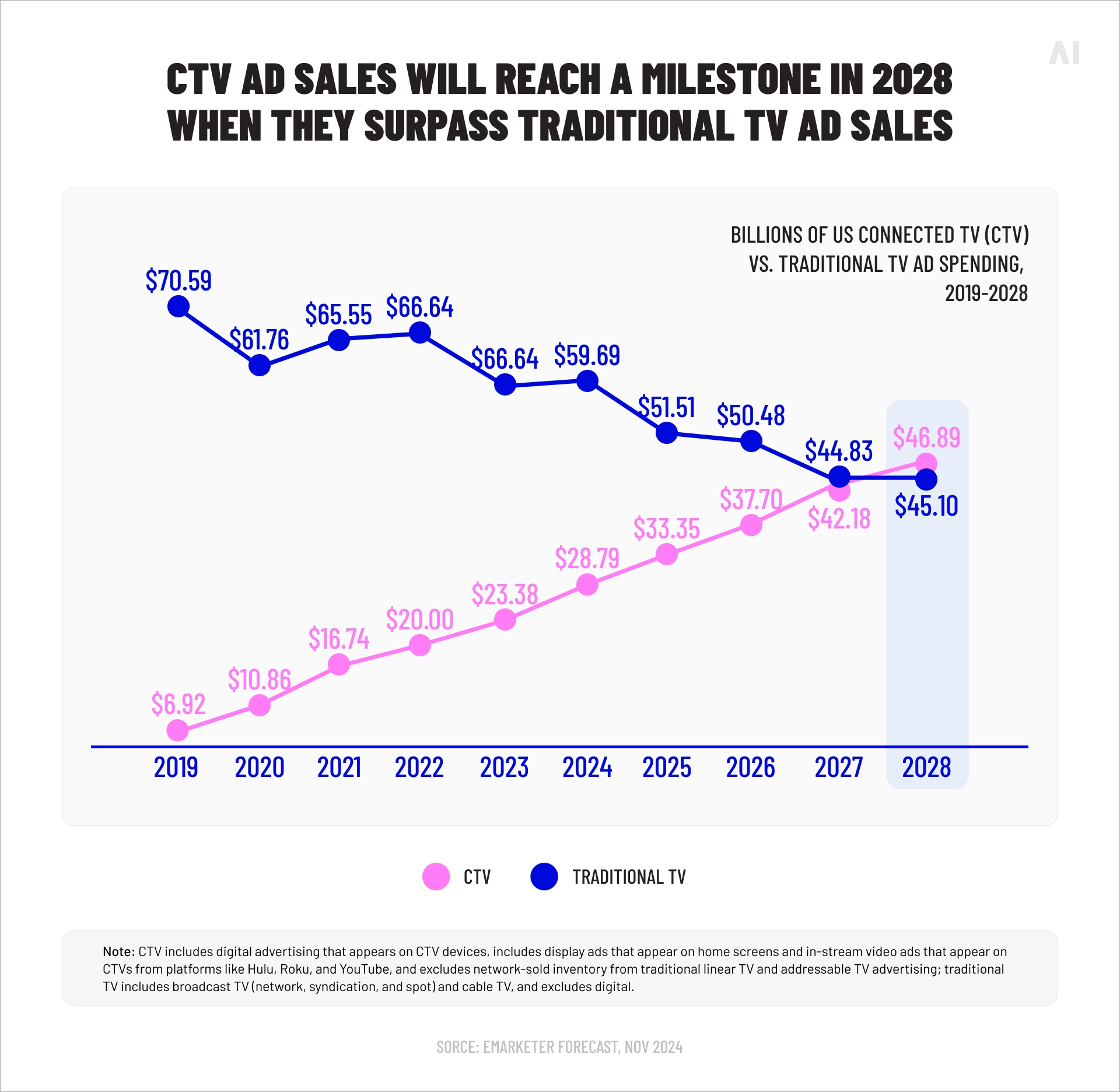

Advertiser demand has followed. In the U.S., digital video ad spend (which includes CTV) grew 18% year over year in 2024 to $64B and is projected to reach $72B in 2025, according to IAB’s two-part 2025 report.

eMarketer separately forecasts U.S. CTV ad spend of about $33.35B in 2025. Together, these signals explain why many publishers have launched or expanded AVOD tiers.

It helps to anchor the model with concrete services. Pure-play AVOD/Free services include Tubi, Pluto TV, The Roku Channel, and Amazon Freevee; Nielsen also lists Tubi, Pluto TV, and Vevo as AVOD examples. Many major SVOD services now run paid ad-supported tiers (e.g., Netflix “with ads,” Disney+ with ads), which are hybrids rather than pure AVOD but operate on the same ad-funded principle.

Pros of AVOD

A short list clarifies why AVOD is attractive to both platforms and marketers.

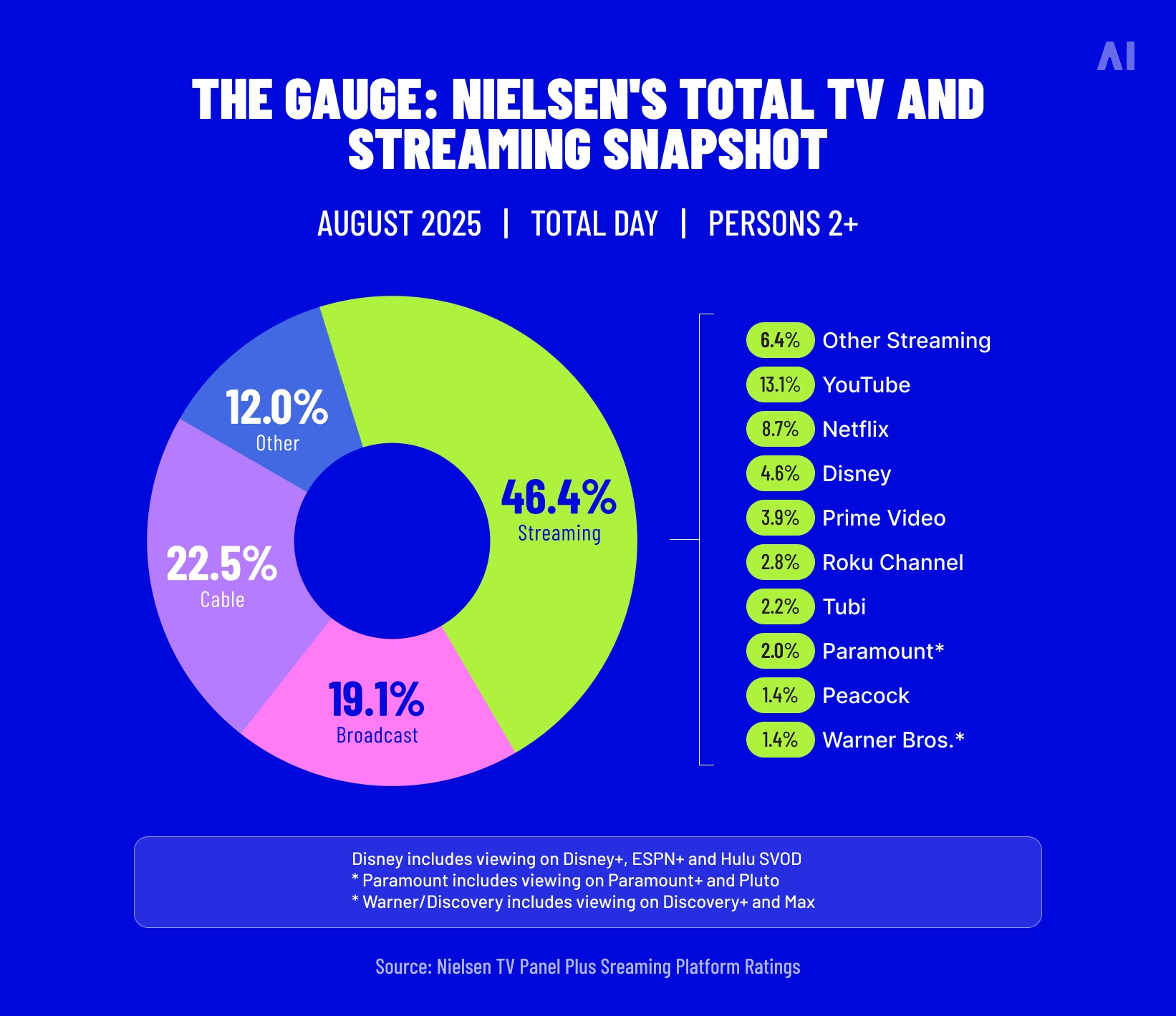

Low barrier, big reach. Removing (or lowering) the subscription fee helps platforms aggregate large, diverse audiences. In the U.S., streaming accounted for ~46.4% of TV time by August 2025, and ad-supported streaming has been the fastest-gaining slice of ad-supported viewing

Budget flexibility. With programmatic pipes, advertisers can start small, test formats, and scale quickly; IAB’s 2025 data shows continued budget migration into digital video and CTV.

Addressability on the big screen. CTV delivers household-level reach with digital-style targeting and measurement, and leading outlooks expect sustained CTV ad growth through the decade.

Resilience in mixed market conditions. When subscription fatigue hits, paid ad-supported services (AVOD tiers) can hold steady even as ad-free SVOD or free FAST categories wobble; Kantar foundAVOD tiers up 0.2% QoQ in Q2 2025 while ad-free SVOD and FAST declined.

⚡ Use AVOD first for fast household reach; layer SVOD ad tiers for quality frequency.

The model also carries trade-offs that teams should plan for.

Ad-load sensitivity and churn risk. Viewers will tolerate ads up to a point; Kantar reported an 8% rise in cancellations due to excessive advertising in Q2 2025, highlighting the need for careful pod design and frequency control.

Fragmentation and transparency challenges. Inventory is spread across many apps and intermediaries, and marketers don’t always control or know the exact content adjacent to their ads—Nielsen flagstransparency, fragmentation, and fraud as ongoing obstacles.

Lower ARPU vs. subscriptions. On a per-user basis, ad-funded revenue typically trails subscription revenue, so platforms often pair AVOD with paid tiers or upsell paths; industry outlooks from PwC and others point to advertising’s growing role in making streaming economics work.

📌 If you’re planning media, the practical read is this: AVOD buys deliver incremental reach at efficient CPMs with digital-level controls, especially on CTV. The catch is to protect user experience—manage frequency, cap pod length, and keep creative relevant—so the audience you gain with free access isn’t lost to avoidable ad fatigue.

What is TVOD?

Transactional video on demand (TVOD) is pay-per-title access. Viewers either rent a title for a short window or buy a permanent digital copy (often called EST—electronic sell-through). TVOD sits alongside SVOD and AVOD but plays a different role: it’s built for new releases, catalog favorites, and one-off viewing without a subscription commitment. Nielsen defines TVOD as on-demand content “on a pay-per-view basis,” distinguishing it from subscription and ad-funded models.

⚡ TVOD shines for event releases—high intent, short windows, no subscription needed.

How TVOD works

Before naming platforms, it helps to see the mechanics. A rental typically gives you 30 days to start and 48 hours to finish once playback begins. Buying (EST) adds the title to your digital library for rewatching on supported devices. Behind the scenes, storefronts support multiple resolutions (SD/HD/4K) and enforce usage rules (e.g., what can be downloaded where) per platform documentation.

⚡ Rentals start the clock; EST buys build your permanent digital library.

Studios also use premium VOD (PVOD)—a higher-priced rental shortly after theatrical release—to capture demand earlier in the window.

U.S. data from the Digital Entertainment Group (DEG) shows internet-delivered digital rentals of new theatricals grew 7.7% YoY in Q3 2024, underscoring this use case.

{{SVOD-AVOD-and-TVOD-SEO-4="/tables"}}

Examples of TVOD platforms

A few mainstream options make the model concrete:

Apple TV app / iTunes Store for renting and buying films and series.

Amazon Prime Video Store for rent/buy alongside subscription content.

YouTube / Google TV for rent/buy on supported devices.

Fandango at Home (formerly Vudu) as a standalone rent/buy storefront.

Pros of TVOD

A short list shows where TVOD earns its keep.

Immediate access to new releases. PVOD and early digital windows let audiences watch current theatrical titles without waiting for subscription availability; DEG’s growth in new-release digital rentals highlights ongoing demand.

High willingness to pay per title. One blockbuster can generate meaningful one-off revenue without long-term subscriber commitments.

No subscription friction. Viewers can dip in for a single film, which complements (rather than competes with) their SVOD mix.

Cons of TVOD

There are also trade-offs—both for platforms and marketers.

Smaller share of total spend. In 2024, U.S. home-entertainment spend was $57.2B, driven largely by subscription streaming; TVOD is a minority slice, which limits scale compared with SVOD.

No recurring revenue. Earnings are hit-driven and variable, and marketing must be concentrated around each title’s release window.

Usage constraints. Rental clocks (30 days to start, ~48 hours to finish) and device rules can limit flexibility for viewers, as platform support pages spell out.

Limited ad inventory. TVOD stores typically don’t run ads inside playback, so brands engage TVOD audiences via off-platform media rather than in-stream placements.

📌 If you’re planning media or distribution, treat TVOD as a transactional spike channel: it’s ideal for event-level demand and premium windows, while SVOD/AVOD carry the day-to-day reach.

Choosing between subscription, ad-funded, and pay-per-title models shapes who pays, what the experience feels like, and how money flows back to the platform. The three aren’t delivery methods (that’s OTT/CTV); they’re monetisation choices that can even coexist inside a single app. Use the side-by-side below to see where avod vs svod vs tvod diverge most.

Payment model

This is how each model handles payment from the viewer:

{{SVOD-AVOD-and-TVOD-SEO-5="/tables"}}

User experience

This is what the viewing experience looks like for each model:

{{SVOD-AVOD-and-TVOD-SEO-6="/tables"}}

Revenue generation

This is how platforms earn money under each model:

{{SVOD-AVOD-and-TVOD-SEO-7="/tables"}}

What this means in practice

In practical terms, these differences create a few clear trade-offs:

Scale vs. yield: AVOD tends to maximise reach quickly; SVOD maximises predictable yield per user; TVOD concentrates revenue around new releases and catalog favourites.

Experience design: SVOD sets quality expectations (especially ad-free); AVOD must balance ad load and frequency; TVOD depends on smooth storefronts and flexible device rules.

Media planning: AVOD delivers efficient incremental reach on CTV; SVOD ad tiers offer premium environments; TVOD is best supported with off-platform media around release windows.

How these models fit into OTT and CTV

It helps to separate what you sell (SVOD, AVOD, TVOD) from how viewers get it (OTT delivery and the CTV screen). The three monetisation models all travel over OTT; CTV is simply the living-room screen where much of that OTT viewing happens.

OTT is the delivery rail

Over-the-top (OTT) services stream over the public internet to phones, tablets, laptops, set-top sticks, consoles, and smart TVs. SVOD, AVOD, and TVOD all live inside OTT apps: a single service can offer an ad-free subscription tier, an ad-supported subscription tier, and a rent/buy store under one roof. Because OTT spans many devices, identity and measurement vary by surface (e.g., device IDs on mobile, household signals on TV, logged-in accounts in apps).

Connected TV (CTV) refers to the TV device (smart TV or TV + streaming stick/console). From a viewer’s perspective, it’s where they open the Netflix, Disney+, Tubi, or Prime Video app. From a marketer’s perspective, it’s where ad-supported experiences (AVOD or SVOD with ads) deliver in-stream TV-style spots with digital controls such as frequency caps, household targeting, and incremental reach alongside or instead of linear TV.

How each model shows up on OTT/CTV

Below is how each model typically appears and operates across OTT apps and on connected TVs.

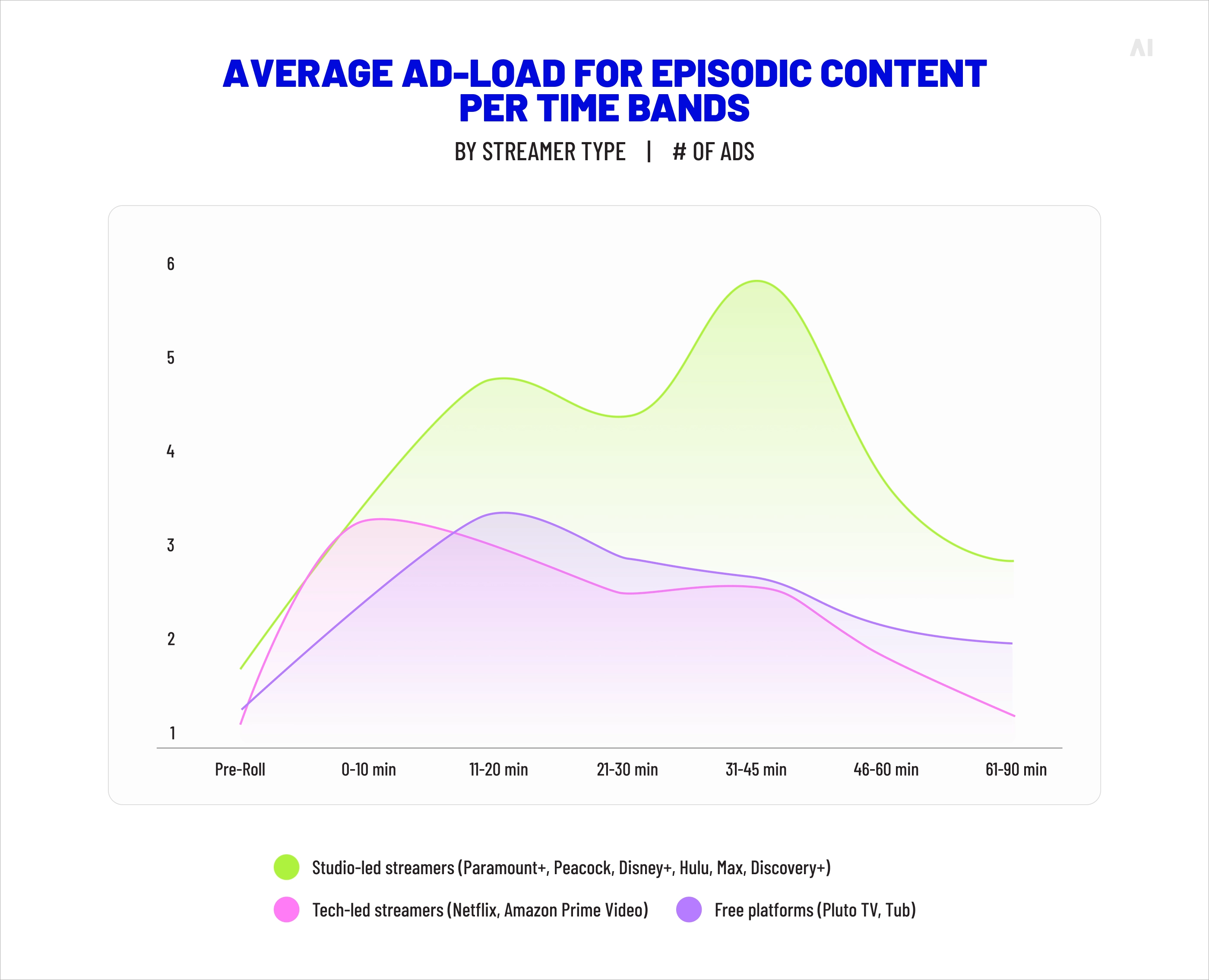

SVOD: Users authenticate and unlock a catalogue. On CTV, ad-free tiers deliver uninterrupted playback; with-ads tiers run fewer, shorter ad pods than linear TV and often use server-side ad insertion (SSAI) for smooth delivery.

AVOD: Content is free or lower cost and funded by advertising. On CTV, dynamic ad insertion stitches pre-, mid-, and post-roll pods into streams; identity is typically household-level, so plans lean on contextual signals, content ratings, and platform first-party segments.

TVOD: Users rent or buy individual titles. On CTV and other OTT devices, TVOD stores usually do not carry in-stream ads, so marketers reach these viewers via off-platform media (e.g., CTV ads on AVOD services) timed to release windows.

⚡ On CTV, identity is household-level—plan creative for lean-back viewing.

Adjacent formats that share the same rails

These formats run on the same OTT/CTV rails as VOD and usually live in the same apps—here’s how they fit.

FAST channels: Free ad-supported streaming TV replicates a channel grid inside OTT apps and is consumed largely on CTV. It’s linear in feel, but delivered over OTT and monetised like AVOD.

vMVPDs: Virtual multichannel bundles (e.g., YouTube TV, Sling TV) stream live channels via OTT to CTV, often paired with on-demand libraries.

Planning implications for marketers

Use the points below to turn model differences into concrete choices for reach, creative, and measurement.

Reach and frequency: AVOD on CTV supplies rapid household reach; SVOD ad tiers add premium inventory without abandoning subscription economics; TVOD needs off-platform support to drive rentals or sales.

Creative and interaction: CTV is lean-back with limited interactivity; use :15–:30s, audio-heavy storytelling, and companion tactics (QR codes, second-screen) to capture response.

Measurement and identity: Expect household-level targeting on CTV, broader identity controls on mobile/desktop OTT, and platform-specific attribution; unify with incrementality testing rather than a single click-through model.

Distribution strategy: Treat OTT as the universal pipe and CTV as the premium screen. Build a mix where AVOD delivers scale, SVOD-with-ads delivers premium adjacency, and TVOD capitalises on event-level demand (e.g., new releases) while the subscription tiers do the heavy lifting day to day.

⚡ Measure incrementality with holdouts or geo splits—don’t rely on last-click.

Benefits of understanding VOD models for marketers

Knowing how SVOD, AVOD, and TVOD actually work helps you plan media and distribution with intent instead of guesswork. The goal is simple: match the audience you want with the experience they value and the revenue path that makes sense for your business.

Choosing the right distribution strategy

Before spending a pound on media or production, decide what outcome you need: reach at scale, premium attention, or high-intent purchases. Each model is a tool for a different job.

Use AVOD when you want fast household reach on connected TV (CTV) and flexible, test-and-learn budgets. Prioritise partners with strong frequency controls and transparent inventory.

Use SVOD ad tiers when you need premium, brand-safe environments with higher completion rates than social video. Treat ad-free SVOD as a loyalty lever for your own app or channel, while ad-supported tiers widen the funnel.

Use TVOD around event moments (new releases, specials, live PPV-style content). Support TVOD with off-platform media on AVOD/CTV to push rentals or buys during the launch window.

Blend models inside one app or plan: ad-supported tiers for acquisition, ad-free for retention, and TVOD for spikes.

Matching content with monetization model

Not every piece of content belongs behind a subscription, and not every title needs ads. Map your slate to the model that fits its demand curve.

High-demand, must-see titles: Monetise first via TVOD or premium windows, then roll into SVOD to drive retention.

Broad, evergreen catalogues: Fit well with AVOD, where depth and variety sustain time spent without heavy promotion.

Series with strong fandom: Anchor in SVOD to reward continuity and reduce churn; use ad tiers for incremental reach.

Short-form and utility content: Often better in AVOD, where snackable viewing aligns with ad-supported habits.

Niche or instructional content with clear value: Consider SVOD micro-subscriptions or bundles; members pay for reliability and depth.

📌 A quick litmus test: if your audience values access, think SVOD; if they value choice without commitment, think AVOD; if they value immediacy for a specific title, think TVOD.

Optimizing ad spend across CTV/OTT

Once the distribution choice is clear, tune buying and measurement so CTV and broader OTT work together rather than in silos.

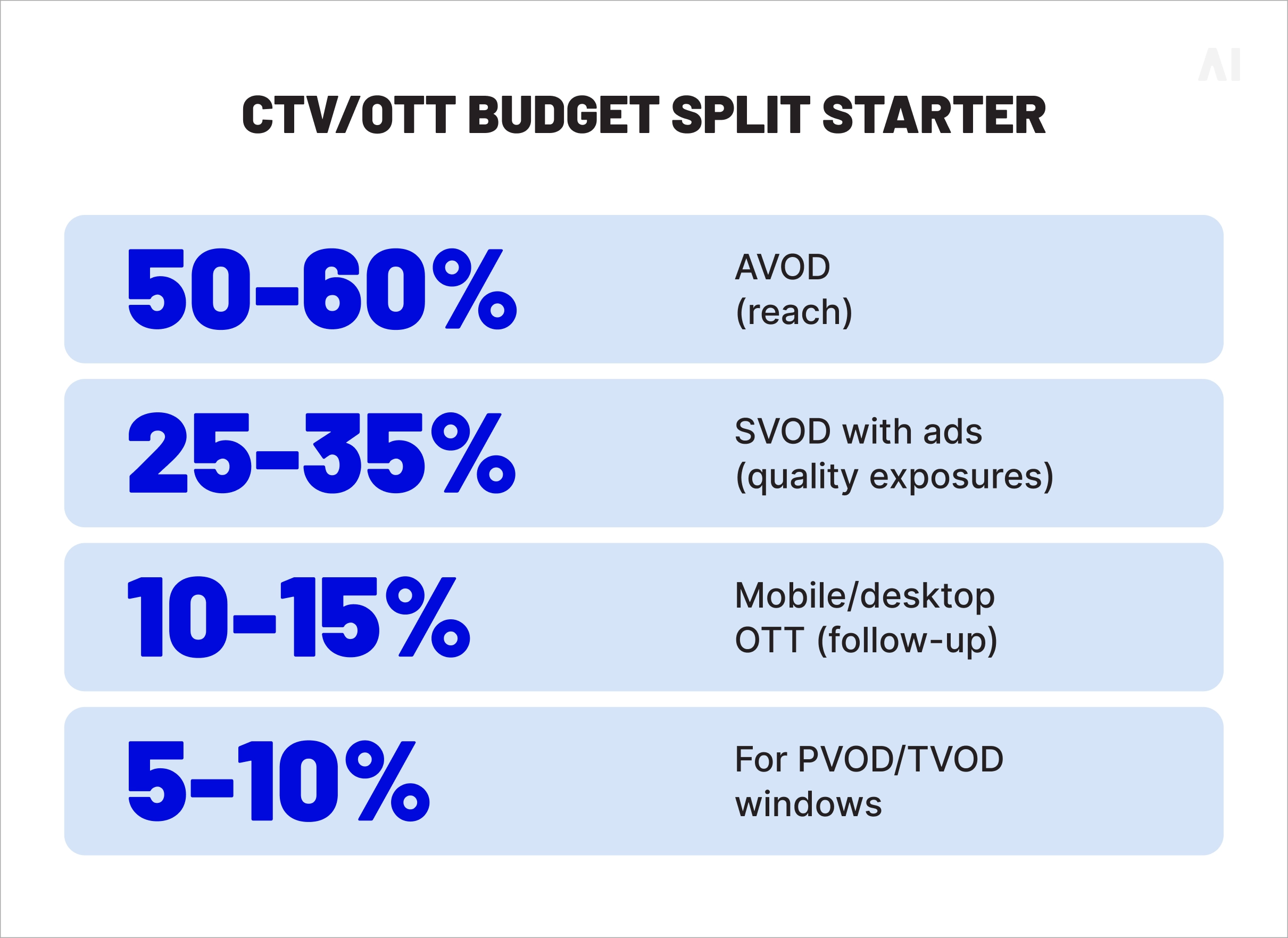

Plan for incremental reach: Start with AVOD on CTV to cover households you can’t reach on linear, then layer SVOD ad tiers for premium frequency.

Right-size frequency: Cap total exposures across apps. Use platform-level frequency tools and creative rotation to avoid ad fatigue.

Match creative to context: Lean-back CTV favours 15s/30s with clear audio cues and a single call to action. Use scannable elements (QR, brand URLs) to bridge TV to mobile.

Measure lift, not just clicks: Run holdout or geography-split tests to quantify incremental reach and outcomes; align to business KPIs (sign-ups, rentals, trials) rather than proxy metrics.

Sequence messaging: Use AVOD for awareness, retarget engaged viewers with mid-funnel formats on OTT/mobile, and close with performance units timed to TVOD windows or SVOD trials.

The next phase of streaming is less about picking a single model and more about mixing models inside the same service to balance reach, revenue, and viewer choice. Three shifts matter most for planning over the next 12–24 months.

Hybrid models (AVOD + SVOD tiers)

Viewers are increasingly opting for paid plans that include ads, while platforms keep premium ad-free tiers for those willing to pay more. That mix widens the funnel without abandoning subscription revenue.

Ad-supported tiers have reached scale. Netflix’s ads plan now exceeds 94 million global monthly active users (MAUs), reflecting rapid adoption in less than two years.

Marketwide, about 46% of US streaming subscribers are on ad-supported plans, driven by sustained price rises and broader tier choices.

By early 2025, US paid ad-tier subscriptions eclipsed 225 million, signaling that hybrid monetization is becoming the default across major services.

Average ad-load for episodic content per time bands by streamer type (Source)

📌 What to do with this: plan media to tap both environments. Use SVOD ad tiers for premium contexts and completion rates, while AVOD supplies incremental household reach on CTV. Keep an eye on tier migration as prices change.

Rise of FAST channels

Free, scheduled streaming channels inside OTT apps keep growing because they reduce choice overload and deliver TV-like simplicity with digital distribution.

Across the US, UK, Canada and Germany, FAST services reached ~1,755 by May 2025, up 17% since June 2024 and 67% since June 2023 (Gracenote data via eMarketer).

Globally, active FAST channels grew nearly 14% from Q1 2025 and 76% since 2023, per Nielsen’s Gracenote unit—evidence that this is not just a US phenomenon.

FAST also rides the broader shift to streaming, which expands ad-supported supply on the big screen..

📌 What to do with this: treat FAST like linear-style reach inside OTT/CTV plans. Use pod strategies and frequency management to avoid fatigue, and pair with VOD ad buys to cover both lean-back and on-demand moments.

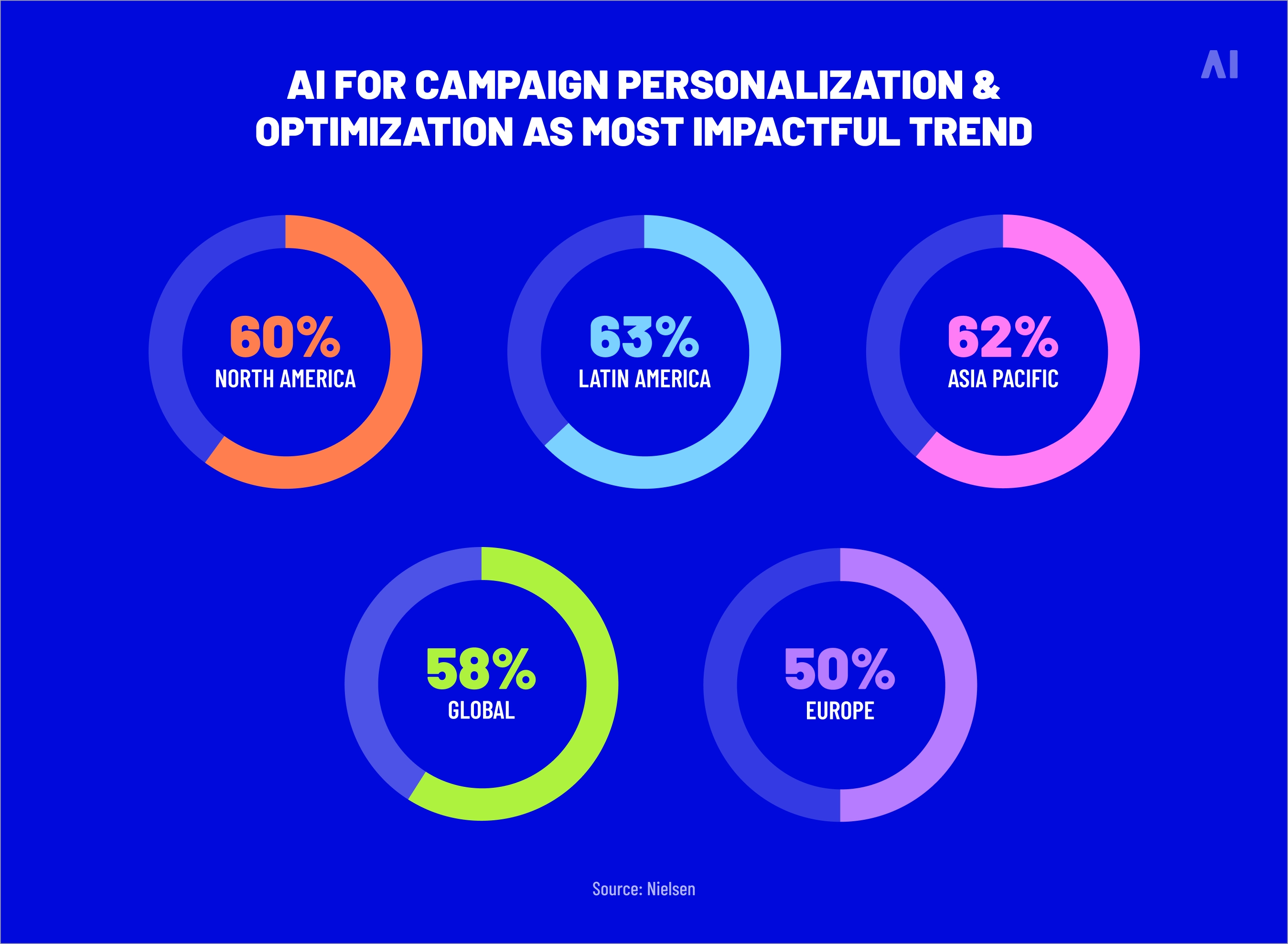

Role of data and AI in targeting

Data and AI are reshaping how inventory is found, bought, measured, and optimized across OTT/CTV.

PwC highlights AI’s growing impact on making advertising more relevant and effective, and links AI to the rise of connected TV advertising over the forecast period.

Nielsen’s 2025 releases underscore the shift to big-data + panel TV measurement (now MRC-accredited in the US), improving person-level accuracy for streaming and CTV.

Marketers themselves report adopting AI for audience segmentation, creative optimization, and measurement, per Nielsen’s annual marketing report and analysis on AI’s role in modern marketing.

Forecasts also show continued CTV in-stream ad growth this cycle, reinforcing the need for outcome-driven buying and smarter identity strategies.

AI for campaign personalization & optimization trend (Source)

📌 What to do with this: consolidate buys around outcome signals, not just surface CPMs. Use solutions that reduce waste in the bidstream, standardize measurement, and route spend toward supply that proves performance.

🎯 For teams that want these improvements without rebuilding their supply stack, Smart Supply focuses on building deal IDs around your KPI outcomes, works DSP-agnostically across display, streaming video, CTV, and audio, and removes inefficient hops in the path to premium supply so more of the budget reaches working media. It can activate quickly (no minimums, revenue-share model with SSPs) and is designed to prioritize performance over platform bias.

Conclusion: which VOD monetization model is right for your strategy?

A useful way to decide is to start with the outcome you need—then pick the model that best supports it. The three models can live side by side in one plan or even one app, so you’re rarely choosing only one path.

When brands should invest in AVOD vs. SVOD vs. TVOD

Use this quick guide to match each model to the outcome you’re chasing:

Choose AVOD when you need fast, efficient reach on the big screen and want to test, learn, and scale. It’s ideal for broad awareness, frequent creative rotation, and household-level targeting on CTV.

Choose SVOD ad tiers when premium context, higher completion rates, and brand safety are priorities, while still benefiting from addressable buying. Keep ad-free SVOD for loyalty and retention plays inside your own app or channel.

Choose TVOD around event moments—new releases, specials, or one-off experiences—then support those windows with AVOD/CTV media that drives rentals or purchases.

Why hybrid models are gaining traction

Here’s why most services and plans now combine paid and ad-supported tiers:

Hybrid line-ups let services meet two needs at once: price-sensitive viewers who are comfortable with ads, and ad-averse viewers who will pay more for quiet playback.

For marketers, hybrids open two doors inside the same service: premium storytelling environments (SVOD with ads) and efficient scale (pure AVOD). Planning becomes about tier mix rather than platform vs. platform.

How to stay competitive in the evolving streaming market

Turn the differences above into a simple operating routine for planning and measurement.

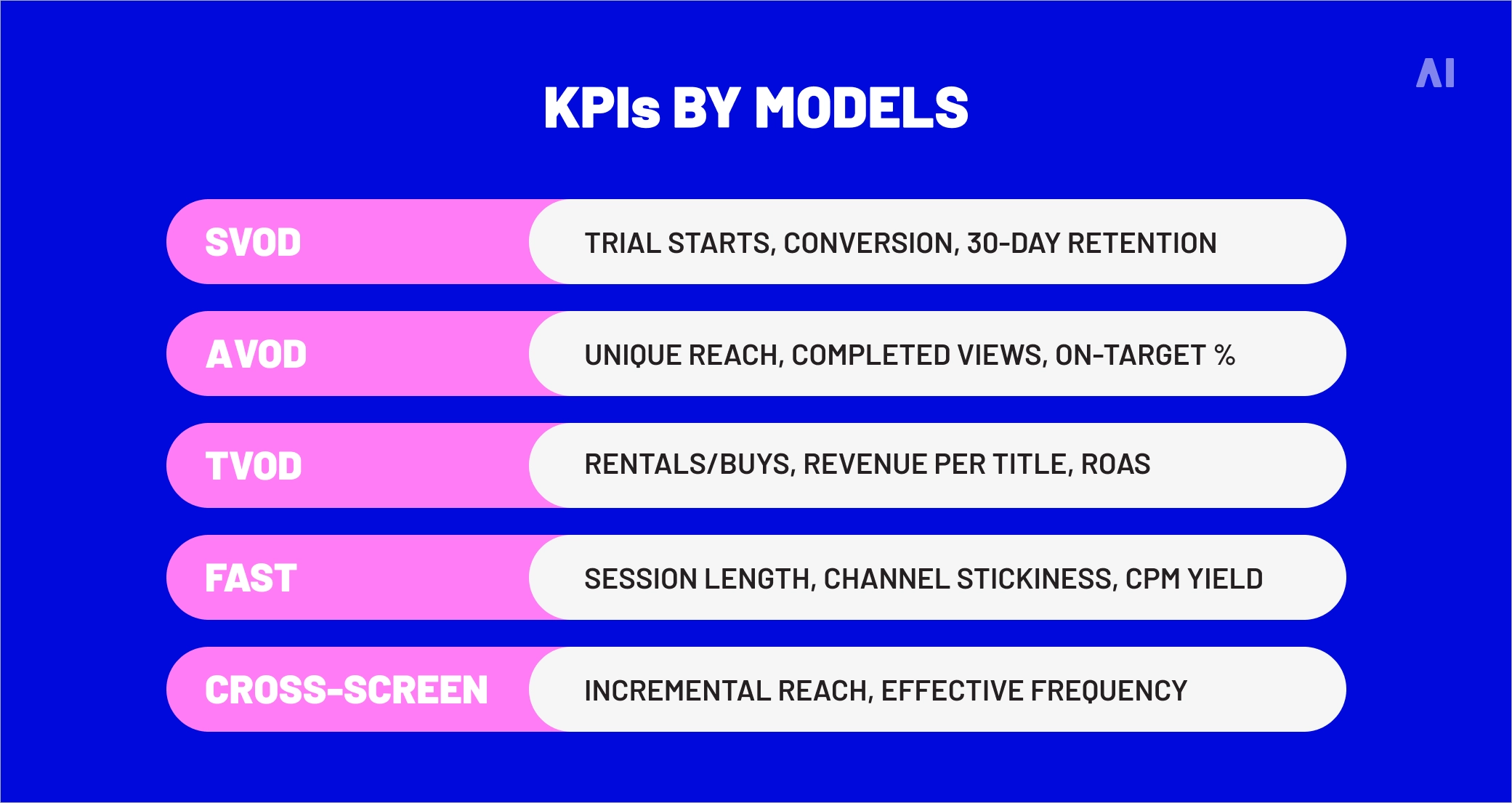

Plan for reach, frequency, and outcome together. Use AVOD for incremental reach on CTV, layer SVOD ad tiers for quality exposures, and align TVOD bursts with product or title launches.

Protect the viewer experience. Set guardrails for total frequency across apps, keep ad pods short, and refresh creative regularly to avoid fatigue.

Sequence your messaging. Start broad on AVOD, retarget engaged viewers with mid-funnel OTT/mobile, and close with performance units tied to a TVOD window or SVOD trial.

Measure incrementality, not just delivery. Run holdouts or geo splits to prove lift on sign-ups, rentals, or sales. Treat last-click as a clue, not the whole story.

Consolidate buying around supply that proves performance. Prioritise partners and deals that consistently hit your KPI, and reduce hops in the path so more budget becomes working media.

If you want a partner to execute this mix with discipline, AI Digital brings DSP-agnostic buying, outcome-based planning, and cross-channel execution (CTV/OTT, video, display, audio, and more). Our Open Garden approach gives you flexibility across platforms; our managed service pairs AI-powered optimisation with human oversight; and our Smart Supply service builds deal IDs around your KPIs and streamlines the route to premium inventory so more of your spend reaches real audiences. Ready to stress-test your plan or build one from scratch? Get in touch!

Blind spot

Key issues

Business impact

AI Digital solution

Lack of transparency in AI models

• Platforms own AI models and train on proprietary data • Brands have little visibility into decision-making • "Walled gardens" restrict data access

• Inefficient ad spend • Limited strategic control • Eroded consumer trust • Potential budget mismanagement

Open Garden framework providing: • Complete transparency • DSP-agnostic execution • Cross-platform data & insights

Optimizing ads vs. optimizing impact

• AI excels at short-term metrics but may struggle with brand building • Consumers can detect AI-generated content • Efficiency might come at cost of authenticity

• Short-term gains at expense of brand health • Potential loss of authentic connection • Reduced effectiveness in storytelling

Smart Supply offering: • Human oversight of AI recommendations • Custom KPI alignment beyond clicks • Brand-safe inventory verification

The illusion of personalization

• Segment optimization rebranded as personalization • First-party data infrastructure challenges • Personalization vs. surveillance concerns

• Potential mismatch between promise and reality • Privacy concerns affecting consumer trust • Cost barriers for smaller businesses

Elevate platform features: • Real-time AI + human intelligence • First-party data activation • Ethical personalization strategies

AI-Driven efficiency vs. decision-making

• AI shifting from tool to decision-maker • Black box optimization like Google Performance Max • Human oversight limitations

• Strategic control loss • Difficulty questioning AI outputs • Inability to measure granular impact • Potential brand damage from mistakes

Managed Service with: • Human strategists overseeing AI • Custom KPI optimization • Complete campaign transparency

Fig. 1. Summary of AI blind spots in advertising

Dimension

Walled garden advantage

Walled garden limitation

Strategic impact

Audience access

Massive, engaged user bases

Limited visibility beyond platform

Reach without understanding

Data control

Sophisticated targeting tools

Data remains siloed within platform

Fragmented customer view

Measurement

Detailed in-platform metrics

Inconsistent cross-platform standards

Difficult performance comparison

Intelligence

Platform-specific insights

Limited data portability

Restricted strategic learning

Optimization

Powerful automated tools

Black-box algorithms

Reduced marketer control

Fig. 2. Strategic trade-offs in walled garden advertising.

Core issue

Platform priority

Walled garden limitation

Real-world example

Attribution opacity

Claiming maximum credit for conversions

Limited visibility into true conversion paths

Meta and TikTok's conflicting attribution models after iOS privacy updates

Data restrictions

Maintaining proprietary data control

Inability to combine platform data with other sources

Amazon DSP's limitations on detailed performance data exports

Cross-channel blindspots

Keeping advertisers within ecosystem

Fragmented view of customer journey

YouTube/DV360 campaigns lacking integration with non-Google platforms

Black box algorithms

Optimizing for platform revenue

Reduced control over campaign execution

Self-serve platforms using opaque ML models with little advertiser input

Performance reporting

Presenting platform in best light

Discrepancies between platform-reported and independently measured results

Consistently higher performance metrics in platform reports vs. third-party measurement

Fig. 1. The Walled garden misalignment: Platform interests vs. advertiser needs.

Key dimension

Challenge

Strategic imperative

ROAS volatility

Softer returns across digital channels

Shift from soft KPIs to measurable revenue impact

Media planning

Static plans no longer effective

Develop agile, modular approaches adaptable to changing conditions

Brand/performance

Traditional division dissolving

Create full-funnel strategies balancing long-term equity with short-term conversion

Capability

Key features

Benefits

Performance data

Elevate forecasting tool

• Vertical-specific insights • Historical data from past economic turbulence • "Cascade planning" functionality • Real-time adaptation

• Provides agility to adjust campaign strategy based on performance • Shows which media channels work best to drive efficient and effective performance • Confident budget reallocation • Reduces reaction time to market shifts

• Dataset from 10,000+ campaigns • Cuts response time from weeks to minutes

• Reaches people most likely to buy • Avoids wasted impressions and budgets on poor-performing placements • Context-aligned messaging

• 25+ billion bid requests analyzed daily • 18% improvement in working media efficiency • 26% increase in engagement during recessions

Full-funnel accountability

• Links awareness campaigns to lower funnel outcomes • Tests if ads actually drive new business • Measures brand perception changes • "Ask Elevate" AI Chat Assistant

• Upper-funnel to outcome connection • Sentiment shift tracking • Personalized messaging • Helps balance immediate sales vs. long-term brand building

• Natural language data queries • True business impact measurement

Open Garden approach

• Cross-platform and channel planning • Not locked into specific platforms • Unified cross-platform reach • Shows exactly where money is spent

• Reduces complexity across channels • Performance-based ad placement • Rapid budget reallocation • Eliminates platform-specific commitments and provides platform-based optimization and agility

• Coverage across all inventory sources • Provides full visibility into spending • Avoids the inability to pivot across platform as you’re not in a singular platform

Fig. 1. How AI Digital helps during economic uncertainty.

Trend

What it means for marketers

Supply & demand lines are blurring

Platforms from Google (P-Max) to Microsoft are merging optimization and inventory in one opaque box. Expect more bundled “best available” media where the algorithm, not the trader, decides channel and publisher mix.

Walled gardens get taller

Microsoft’s O&O set now spans Bing, Xbox, Outlook, Edge and LinkedIn, which just launched revenue-sharing video programs to lure creators and ad dollars. (Business Insider)

Retail & commerce media shape strategy

Microsoft’s Curate lets retailers and data owners package first-party segments, an echo of Amazon’s and Walmart’s approaches. Agencies must master seller-defined audiences as well as buyer-side tactics.

AI oversight becomes critical

Closed AI bidding means fewer levers for traders. Independent verification, incrementality testing and commercial guardrails rise in importance.

Fig. 1. Platform trends and their implications.

Metric

Connected TV (CTV)

Linear TV

Video Completion Rate

94.5%

70%

Purchase Rate After Ad

23%

12%

Ad Attention Rate

57% (prefer CTV ads)

54.5%

Viewer Reach (U.S.)

85% of households

228 million viewers

Retail Media Trends 2025

Access Complete consumer behaviour analyses and competitor benchmarks.

Identify and categorize audience groups based on behaviors, preferences, and characteristics

Michaels Stores: Implemented a genAI platform that increased email personalization from 20% to 95%, leading to a 41% boost in SMS click through rates and a 25% increase in engagement.

Estée Lauder: Partnered with Google Cloud to leverage genAI technologies for real-time consumer feedback monitoring and analyzing consumer sentiment across various channels.

High

Medium

Automated ad campaigns

Automate ad creation, placement, and optimization across various platforms

Showmax: Partnered with AI firms toautomate ad creation and testing, reducing production time by 70% while streamlining their quality assurance process.

Headway: Employed AI tools for ad creation and optimization, boosting performance by 40% and reaching 3.3 billion impressions while incorporating AI-generated content in 20% of their paid campaigns.

High

High

Brand sentiment tracking

Monitor and analyze public opinion about a brand across multiple channels in real time

L’Oréal: Analyzed millions of online comments, images, and videos to identify potential product innovation opportunities, effectively tracking brand sentiment and consumer trends.

Kellogg Company: Used AI to scan trending recipes featuring cereal, leveraging this data to launch targeted social campaigns that capitalize on positive brand sentiment and culinary trends.

High

Low

Campaign strategy optimization

Analyze data to predict optimal campaign approaches, channels, and timing

DoorDash: Leveraged Google’s AI-powered Demand Gen tool, which boosted its conversion rate by 15 times and improved cost per action efficiency by 50% compared with previous campaigns.

Kitsch: Employed Meta’s Advantage+ shopping campaigns with AI-powered tools to optimize campaigns, identifying and delivering top-performing ads to high-value consumers.

High

High

Content strategy

Generate content ideas, predict performance, and optimize distribution strategies

JPMorgan Chase: Collaborated with Persado to develop LLMs for marketing copy, achieving up to 450% higher clickthrough rates compared with human-written ads in pilot tests.

Hotel Chocolat: Employed genAI for concept development and production of its Velvetiser TV ad, which earned the highest-ever System1 score for adomestic appliance commercial.

High

High

Personalization strategy development

Create tailored messaging and experiences for consumers at scale

Stitch Fix: Uses genAI to help stylists interpret customer feedback and provide product recommendations, effectively personalizing shopping experiences.

Instacart: Uses genAI to offer customers personalized recipes, mealplanning ideas, and shopping lists based on individual preferences and habits.

Medium

Medium

Share article

Url copied to clipboard

No items found.

Subscribe to our Newsletter

THANK YOU FOR YOUR SUBSCRIPTION

Oops! Something went wrong while submitting the form.

Questions? We have answers

What is the main difference between SVOD and AVOD?

SVOD charges a recurring fee for catalogue access and is typically ad-free at the premium tier, while AVOD is free or lower-priced and funded by in-stream advertising. In short, SVOD monetises primarily through subscriptions; AVOD monetises through ads shown during playback.

Which VOD model is the most profitable?

It depends on your content, audience size, and cost base. SVOD can deliver stable, recurring revenue but must fight churn and fund ongoing content. TVOD can yield high per-title returns around big releases but is hit-driven and volatile. AVOD scales quickly with broad reach, though ARPU is usually lower than subscriptions; it shines when you have depth of catalogue and strong ad sales.

Is Apple TV SVOD or TVOD?

Apple TV is the app and device ecosystem. Apple TV+ inside it is an SVOD service (subscription access to originals), while the Apple TV/iTunes Store offers TVOD (rent or buy individual titles). Many users engage with both in the same interface.

What are FAST channels and how do they relate to VOD?

FAST (free ad-supported streaming TV) channels are linear, scheduled streams delivered over the internet inside OTT apps. They feel like traditional channels but are funded by ads and accessed alongside on-demand catalogues. They sit next to VOD rather than replacing it—viewers can flip between a channel and on-demand titles in the same app.

Are AVOD and OTT the same?

No. AVOD is a business model (ad-funded on-demand). OTT describes delivery (streamed over the internet to any device). AVOD services run over OTT, and many are watched on connected TVs, but AVOD and OTT are not interchangeable terms.

Is Amazon Prime SVOD or TVOD?

Prime Video includes both. The Prime membership unlocks an SVOD catalogue, and the Prime Video Store lets anyone rent or buy individual films and shows (TVOD). One service, two monetisation paths.

Is YouTube AVOD or FVOD?

Core YouTube is free to watch and funded by ads, so it’s commonly labelled FVOD (free VOD) and functionally operates as AVOD. YouTube also offers YouTube Premium (SVOD, ad-free access and extras) and YouTube Movies & Shows (TVOD, rent/buy).

Have other questions?

If you have more questions, contact us so we can help.

Questions? We have answers

This is some text inside of a div block.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique. Duis cursus, mi quis viverra ornare, eros dolor interdum nulla, ut commodo diam libero vitae erat. Aenean faucibus nibh et justo cursus id rutrum lorem imperdiet. Nunc ut sem vitae risus tristique posuere.

This is some text inside of a div block.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique. Duis cursus, mi quis viverra ornare, eros dolor interdum nulla, ut commodo diam libero vitae erat. Aenean faucibus nibh et justo cursus id rutrum lorem imperdiet. Nunc ut sem vitae risus tristique posuere.

This is some text inside of a div block.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique. Duis cursus, mi quis viverra ornare, eros dolor interdum nulla, ut commodo diam libero vitae erat. Aenean faucibus nibh et justo cursus id rutrum lorem imperdiet. Nunc ut sem vitae risus tristique posuere.

This is some text inside of a div block.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique. Duis cursus, mi quis viverra ornare, eros dolor interdum nulla, ut commodo diam libero vitae erat. Aenean faucibus nibh et justo cursus id rutrum lorem imperdiet. Nunc ut sem vitae risus tristique posuere.

This is some text inside of a div block.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique. Duis cursus, mi quis viverra ornare, eros dolor interdum nulla, ut commodo diam libero vitae erat. Aenean faucibus nibh et justo cursus id rutrum lorem imperdiet. Nunc ut sem vitae risus tristique posuere.

This is some text inside of a div block.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique. Duis cursus, mi quis viverra ornare, eros dolor interdum nulla, ut commodo diam libero vitae erat. Aenean faucibus nibh et justo cursus id rutrum lorem imperdiet. Nunc ut sem vitae risus tristique posuere.

This is some text inside of a div block.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique. Duis cursus, mi quis viverra ornare, eros dolor interdum nulla, ut commodo diam libero vitae erat. Aenean faucibus nibh et justo cursus id rutrum lorem imperdiet. Nunc ut sem vitae risus tristique posuere.

.webp)

.svg)

.svg)