Digital Advertising Ecosystem: How It Actually Works in a Fragmented, Platform-Driven World

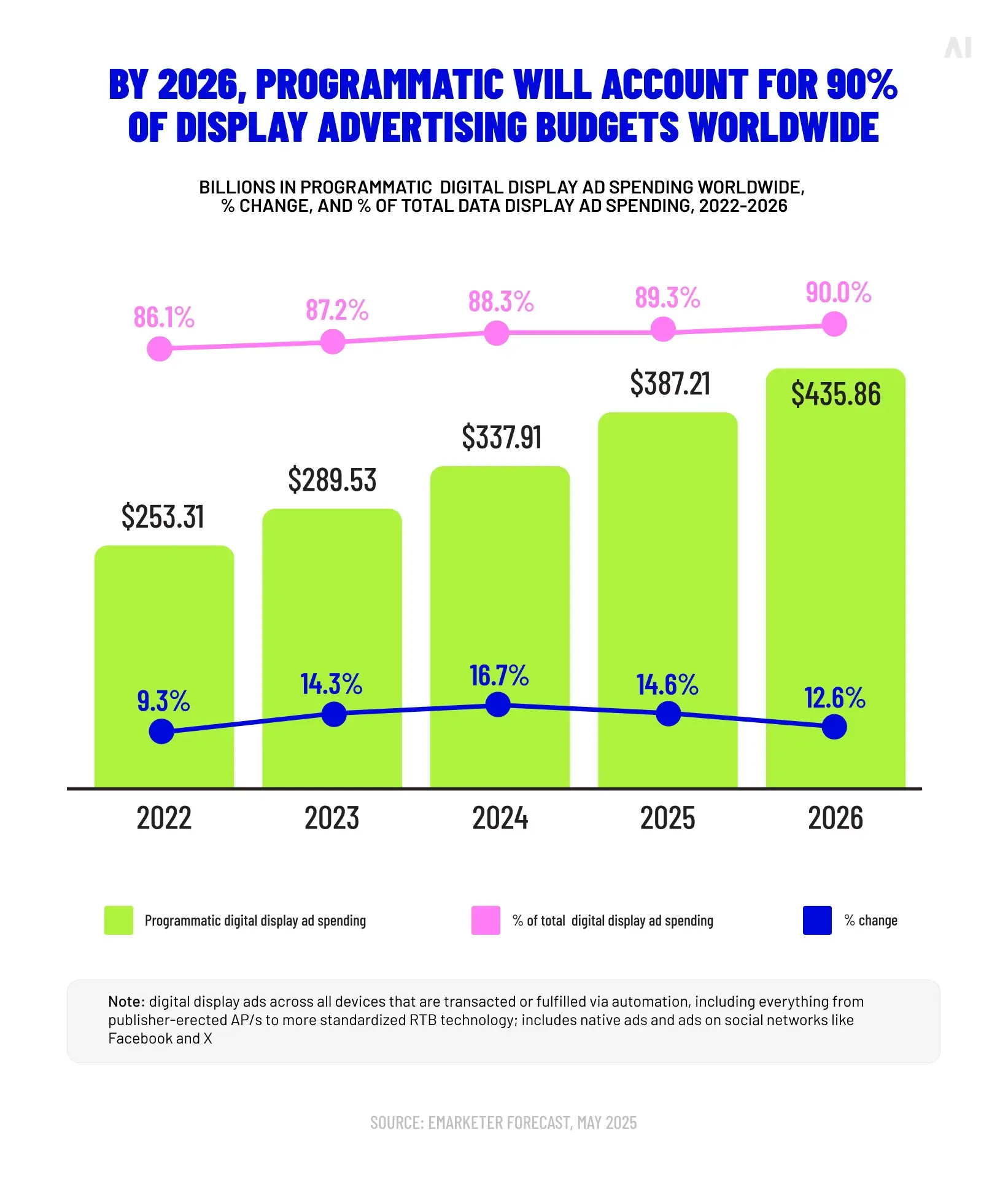

The digital advertising ecosystem is not what it was designed to be. What began as a direct relationship between advertisers and publishers—a brand wanted an audience, a publisher had one—has evolved into a layered, automated, and often opaque system of platforms, intermediaries, and competing data environments. In the United States alone, programmatic ad spending surpassed $270 billion in 2025, accounting for roughly 85% of all digital ad expenditure. That scale did not arrive without trade-offs. The same automation that unlocked speed and precision also introduced fragmentation, duplicated processes, and a structural imbalance in who controls the data, the inventory, and the measurement.

Understanding the digital advertising ecosystem today means understanding where control sits, how value moves between participants, and why the ad tech ecosystem structure so often works against the advertisers funding it. This article breaks down each layer of that system, traces the path of a single ad transaction, and examines the structural challenges that define the fragmented digital advertising landscape in 2026.

What is the digital advertising ecosystem?

The digital advertising ecosystem is the interconnected network of platforms, technologies, data systems, and stakeholders that enable the automated buying and selling of ad inventory across digital channels. It includes demand-side platforms (DSPs), supply-side platforms (SSPs), ad exchanges, data providers, verification vendors, measurement tools, and the advertisers and publishers who operate at either end.

A common misconception is that this ecosystem functions as a linear supply chain—advertiser hands money to a platform, platform delivers an ad to a user, publisher collects revenue. In practice, the ad ecosystem operates more like a dynamic web, where multiple platforms interact simultaneously, often in competition with one another, during a single transaction that resolves in under 100 milliseconds. Real-time decisioning sits at the centre of everything: which user to target, which inventory to bid on, how much to pay, and which creative to serve. Each of those decisions is mediated by a platform with its own commercial incentives.

The result is a system defined less by collaboration than by platform-level control. The platforms that own the richest data, the most desirable inventory, and the most widely adopted measurement tools hold disproportionate influence over how advertising budgets are allocated, optimized, and reported.

{{26-Digital-Advertising-Ecosystem-1="/tables"}}

How programmatic infrastructure powers the ecosystem

Programmatic advertising is not a channel. It is the operational backbone of the digital advertising ecosystem, the infrastructure that connects buyers, sellers, data, and inventory through automated processes and real-time auctions.

At its core, programmatic automates the decisions that media buyers once made manually: which impressions to purchase, at what price, and for which audience. Through real-time bidding (RTB), these transactions happen at the moment a user loads a page or opens an app. A bid request is generated, sent to multiple potential buyers simultaneously, and resolved in the time it takes the page to render. The winning ad appears. The losing bids disappear without a trace.

This infrastructure enables scale that manual buying never could. But scale introduced its own problems. As programmatic matured, layers of intermediaries accumulated between the advertiser's dollar and the publisher's page. Each layer—whether a data provider, a verification vendor, or an additional exchange—takes a fee, adds latency, and reduces the share of spend that reaches the consumer. The ANA's Q4 2025 Programmatic Transparency Benchmark confirmed that advertisers enforcing disciplined quality governance converted 56.7% of their programmatic spend into benchmark-qualified impressions, while lower-performing advertisers managed just 37.5%. The gap between those two figures is the difference between treating programmatic as infrastructure to be governed and treating it as a black box to be tolerated.

💡 Related read: What is programmatic advertising?

The core components of the ecosystem

The programmatic advertising ecosystem is built on several interlocking layers, each with a distinct function in enabling ad delivery. These layers do not operate in isolation; value and control flow between them in ways that shape campaign outcomes, cost efficiency, and strategic flexibility.

Demand side

The demand side is where campaigns are planned, budgets are allocated, and buying decisions are executed. Demand-side platforms (DSPs) are the primary buying interfaces, allowing advertisers and agencies to set targeting parameters, define bid strategies, and purchase inventory across multiple sources from a single platform.

Automation drives most of the demand-side workflow. Machine learning models evaluate bid requests, score available impressions against the advertiser's objectives, and make purchase decisions in real time. The sophistication of these models varies considerably between platforms, and the degree of control advertisers retain over those decisions varies even more. Some DSPs offer granular transparency into bidding logic and inventory sources. Others operate as closed systems where the advertiser defines objectives and the platform handles execution with limited visibility into how decisions are made.

The demand side also includes agency trading desks, managed service providers, and the growing category of AI-powered planning tools that sit above the DSP layer. These tools aim to solve a persistent demand-side problem: managing multiple DSPs, normalizing fragmented performance signals, and making cross-platform budget decisions without the operational overhead that typically requires.

Programmatic was supposed to give marketers the freedom to reach audiences anywhere online by combining data, automation, and inventory from across the web. Instead, the ecosystem has steadily moved in the opposite direction. — Stephen Magli, CEO & Founder, AI Digital (AdExchanger)

💡 Related read: What is a demand-side platform?

Supply side

The supply side is where publishers manage their inventory, set pricing floors, and determine which demand sources can access their ad placements. Supply-side platforms (SSPs) are the primary tool for this, functioning as the publisher's counterpart to the DSP. An SSP connects a publisher's inventory to multiple ad exchanges and DSPs, enabling competition for each impression.

Supply is not passive. Publishers make active decisions about how their inventory is structured, priced, and routed. Premium publishers increasingly use private marketplace (PMP) deals to control who can buy their inventory and at what price. According to the ANA's Q2 2025 benchmark, PMP transactions accounted for nearly 88% of all programmatic spend among participating advertisers, up from 64.5% the previous quarter. That shift reflects a supply side that is becoming more curated, not less.

Supply path optimization (SPO) has also emerged as a critical discipline. The same impression can travel through multiple SSPs, each adding a fee layer before it reaches the buyer. Reducing those hops—eliminating indirect paths, consolidating SSP relationships, and prioritising direct publisher connections—is now a measurable driver of cost efficiency.

Marketplaces and ad exchanges

Ad exchanges are the transaction layer where demand and supply meet. They facilitate the auction mechanics that determine which ad is served to which user at which price. Three primary deal structures operate across these marketplaces.

- Open auctions are the broadest form of programmatic buying. Any eligible buyer can participate, and inventory is available to the widest possible pool of demand. Open auctions offer scale but limited control over where ads appear and which supply paths are used.

- Private marketplaces (PMPs) restrict participation to a curated set of buyers, typically with negotiated pricing floors. PMPs give publishers more control over who accesses their inventory and give buyers more confidence in placement quality.

- Programmatic guaranteed deals remove the auction entirely. The buyer and seller agree on a fixed price and reserved inventory, executed through programmatic pipes. These deals combine the predictability of direct buying with the automation of programmatic delivery.

{{26-Digital-Advertising-Ecosystem-2="/tables"}}

The balance between these structures is shifting. As mentioned previously, PMPs have grown to dominate spend among the most sophisticated buyers, driven by a desire for inventory quality, brand safety, and supply path transparency.

Data layer

Data is the connective tissue of the ecosystem. It enables targeting, powers optimization, informs measurement, and increasingly determines which platforms hold strategic advantage.

- First-party data—information collected directly from customers through owned channels—has grown in strategic importance as third-party cookies face deprecation and privacy regulations tighten. Brands that can activate their own customer data effectively gain a targeting advantage that is not dependent on any single platform's data policies.

- Third-party data, once the default targeting fuel, is in structural decline. Browser-level restrictions, state-level privacy laws, and consumer opt-out mechanisms have all reduced its reliability.

Contextual targeting, which places ads based on the content environment rather than user identity, has re-emerged as a viable alternative, with adoption rising substantially between 2022 and 2025 across the US market.

The fragmentation problem is most acute in the data layer. Each platform operates its own data environment, with limited interoperability between them. An advertiser running campaigns across Google, Meta, Amazon, The Trade Desk, and a CTV platform will receive five separate data sets, five separate attribution models, and five separate versions of what "success" looks like. Unifying those signals into a coherent view of performance remains one of the ecosystem's most persistent and expensive challenges.

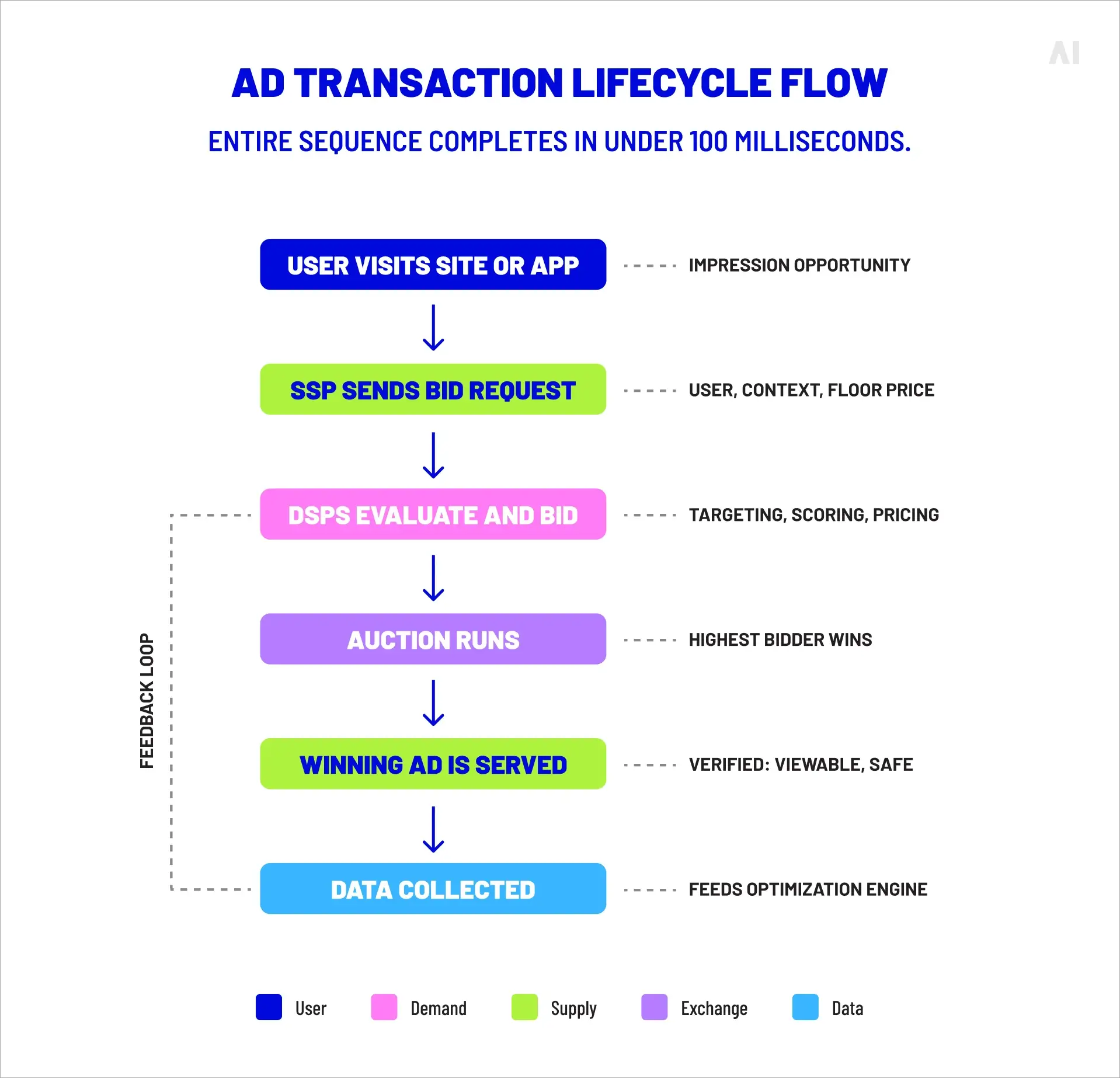

How a single ad transaction actually works (step-by-step)

The complexity of the digital advertising ecosystem becomes more concrete when you trace the path of a single impression from the moment a user arrives on a page to the moment an ad renders on their screen.

Step 1: A user visits a website or opens an app. The publisher's ad server recognizes an available ad placement and initiates a request.

Step 2: The SSP generates a bid request. This request contains information about the user (to the extent privacy settings allow), the content environment, the placement specifications, and the publisher's pricing floor. The bid request is sent to multiple DSPs simultaneously.

Step 3: DSPs evaluate the opportunity. Each DSP that receives the bid request runs it through its decisioning engine: matching the user against the advertiser's targeting criteria, assessing the inventory quality, calculating a bid price based on the campaign's objectives and remaining budget. This entire process happens within milliseconds.

Step 4: The auction runs. Bids are submitted to the exchange. In a first-price auction (the dominant model since 2019), the highest bidder wins and pays the price they submitted. The exchange deducts its fee and passes revenue to the SSP and publisher.

Step 5: The winning ad is served. The creative is delivered to the user's browser or app. Verification vendors confirm that the impression was viewable, fraud-free, and brand-safe. Measurement pixels fire to record the event.

Step 6: Data is collected. The impression, along with any subsequent user action (click, visit, conversion), is logged and fed back into the DSP's optimization engine. That data informs future bidding decisions, completing the feedback loop.

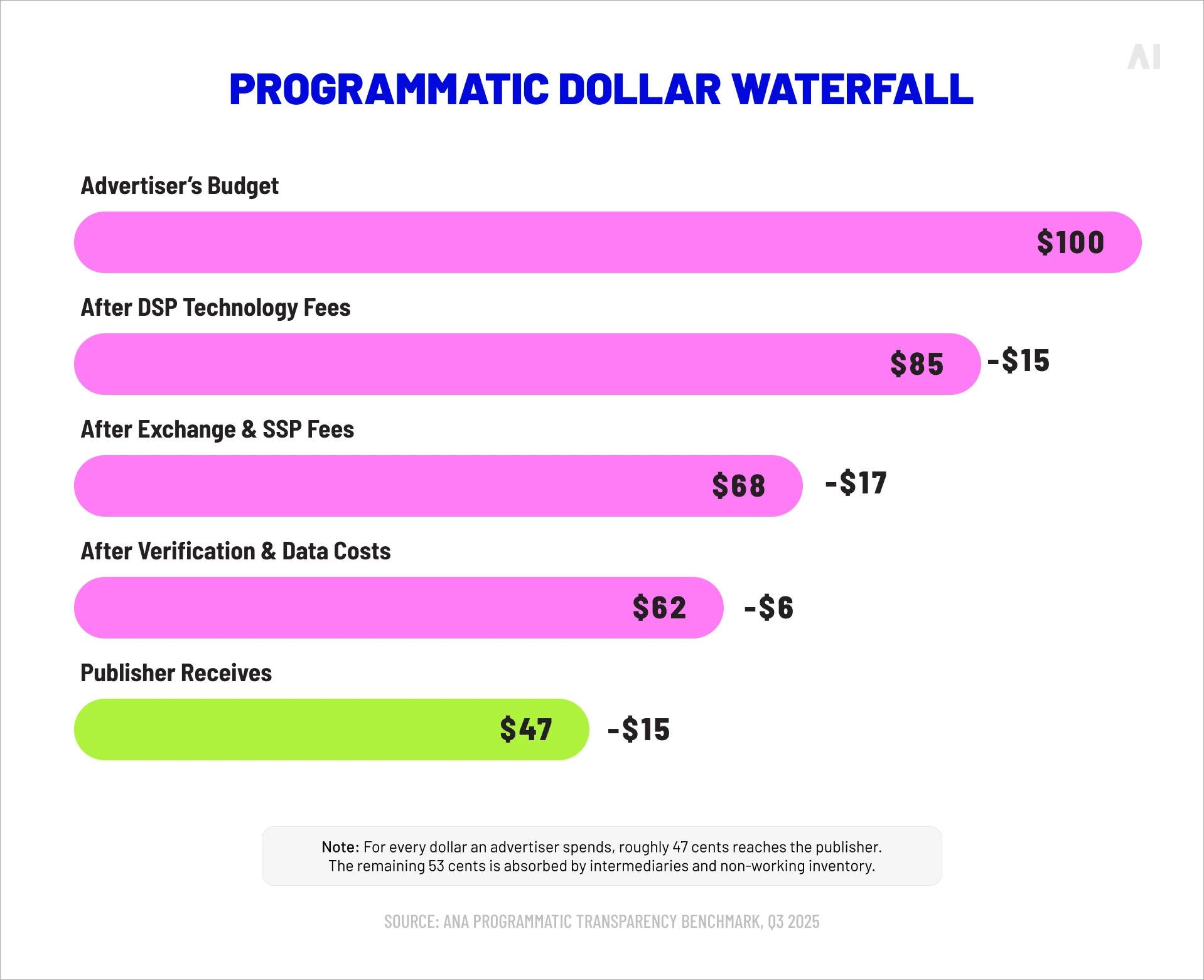

What this sequence does not capture is the number of intermediaries involved. Between the advertiser's budget and the publisher's page, the same impression may pass through an agency, a trading desk, a DSP, one or more exchanges, an SSP, verification vendors, and data providers. Each participant extracts value. The ANA's Q3 2025 benchmark found that the share of ad spend reaching publishers had risen to 47.1%, up 11 points since 2023—an improvement, but one that still means more than half of every programmatic dollar is consumed by the infrastructure between buyer and seller.

Why the ecosystem is fragmented and platform-driven

Fragmentation in the digital advertising ecosystem is not accidental. It is the natural result of independent platforms growing, competing, and building proprietary systems that maximise their own commercial position.

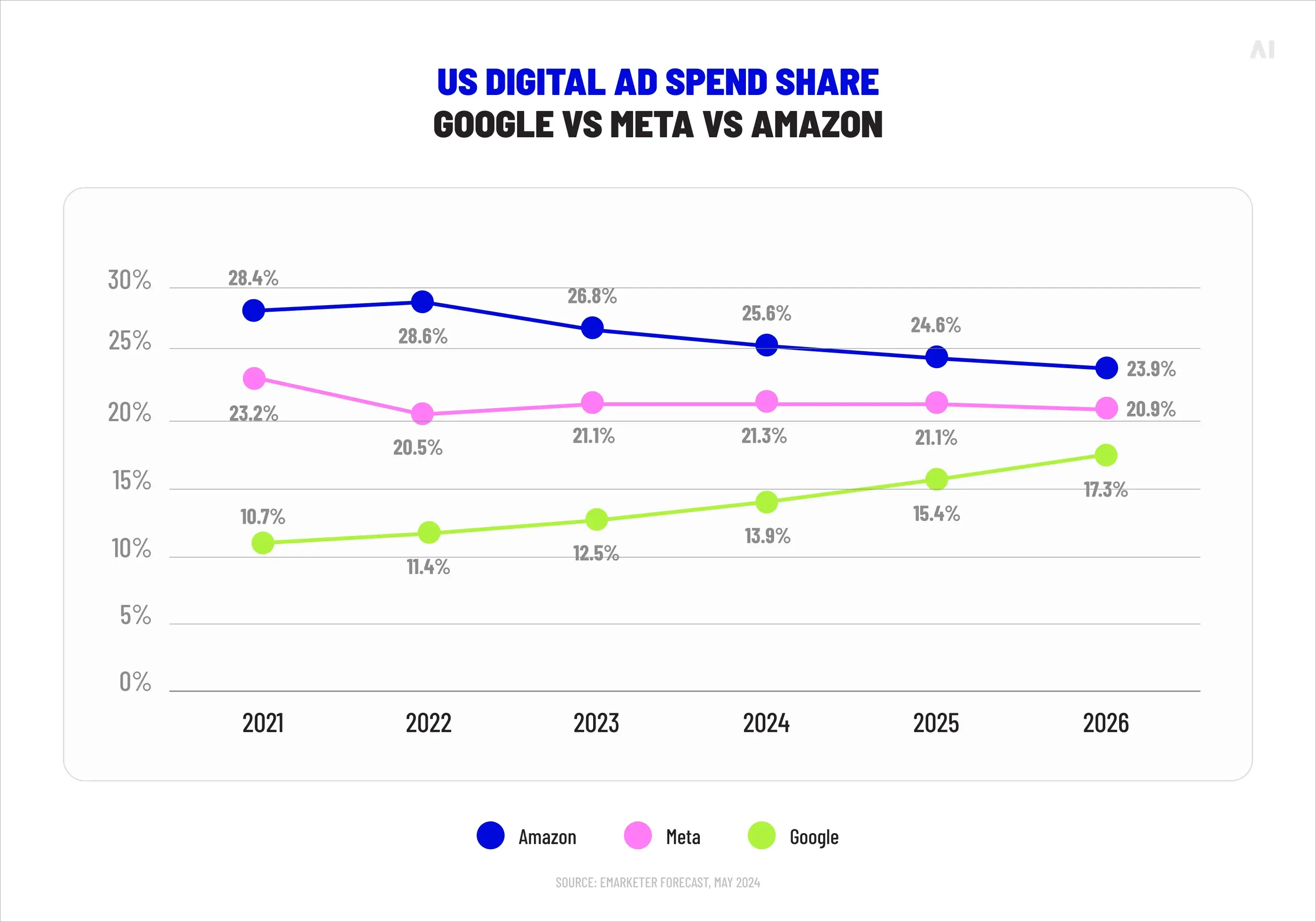

The most visible manifestation of this dynamic is the walled garden. Google, Meta, and Amazon collectively captured approximately 55.8% of the US ad market in 2025. These platforms operate as self-contained environments where the data, the inventory, the targeting tools, and the measurement all remain under platform control. Advertisers can access them, but only through the platform's own interfaces, with the platform's own metrics, on the platform's own terms.

The open internet exists alongside these walled gardens, offering a wider range of inventory, more flexibility in data and targeting, and the potential for cross-platform transparency. But the open internet has its own fragmentation. There are different DSPs for different channels, separate buying paths for CTV and retail media, platform-specific data policies, and an expanding roster of tools required just to maintain reach across the landscape.

{{26-Digital-Advertising-Ecosystem-3="/tables"}}

Each new channel, each new platform, each new data regulation adds another layer to an already complex system. And because each of these layers was built independently, with its own data schema, its own optimization logic, and its own reporting methodology, stitching them together into a coherent operating model is now one of the most expensive and time-consuming challenges in modern marketing.

Transparency that stops at the demand layer is incomplete. If the industry is serious about accountability, supply deserves a far more central role in the conversation. — Britany Scott, VP of Growth, Smart Supply at AI Digital (AI Digital)

💡 Related read: Understanding walled gardens in digital advertising

Structural challenges of the ecosystem

The challenges facing the programmatic advertising ecosystem are not isolated problems. They are interconnected symptoms of a system that grew faster than its governance structures could keep pace with.

- Data silos are the most foundational issue. Every major platform maintains its own data environment with limited portability. An advertiser's audience data inside Google cannot be combined with their audience data inside Meta, which cannot be reconciled with their CTV data from a streaming platform. The result is a fragmented customer view where no single source tells the complete story. Brands invest heavily in data clean rooms, customer data platforms (CDPs), and identity resolution tools to bridge these gaps, but the interoperability challenge remains structurally unresolved.

- Measurement complexity follows directly from data fragmentation. Each platform uses its own attribution methodology, its own counting standards, and its own definition of a conversion. Meta and Google will both claim credit for the same sale. CTV platforms report view-through conversions on timelines that differ from display. Cross-platform measurement frameworks exist, but they require significant investment, technical sophistication, and ongoing maintenance to operate. For most mid-market advertisers, unified measurement remains aspirational rather than operational.

- Operational burden compounds the problem. Managing campaigns across multiple DSPs, reconciling reporting from different platforms, maintaining separate creative workflows for each channel, and coordinating data strategies across siloed environments consumes resources that could be directed toward strategy and creative. The ANA's benchmarks have documented this burden: median SSP counts among participating advertisers fell from 19 to 17 and active domains dropped by nearly half between benchmarking periods, reflecting a deliberate effort to reduce complexity, though the baseline complexity remains high.

- Limited transparency across the supply chain means advertisers often cannot see the full path their budget travels, the fees extracted at each stage, or the logic behind platform-level optimization decisions. The MRC's 2026 Digital Advertising Auction Transparency Standards now require auctioneers to disclose technical fees, bid multipliers, and supply-chain intermediaries, a regulatory signal that the industry recognizes this opacity as a structural problem, not merely a commercial preference.

{{26-Digital-Advertising-Ecosystem-4="/tables"}}

Economic and control dynamics

The economics of the ad ecosystem are shaped by who captures value at each stage of the transaction—and how much of the advertiser's original investment actually reaches the consumer.

- Platform take rates and hidden fees are a persistent concern. Vertically integrated platforms that control both the buying and selling layers of the programmatic stack have a commercial incentive to prioritise their own inventory and extract higher fees at the auction layer. Independent research has estimated that vertical integration can push advertiser costs approximately 20% above the true auction price—a premium that scales with spend and remains invisible to most buyers.

- Intermediaries and duplicated processes erode efficiency further. Ad verification, brand safety, viewability measurement, fraud detection, and identity resolution each come with their own vendor, their own fee, and their own integration requirements. Many of these functions overlap, creating duplicated costs for capabilities that could be consolidated.

- Supply path inefficiencies remain one of the largest sources of waste. When the same impression is available through multiple SSPs, each adding its own fee layer, the buyer pays more than necessary for inventory that could have been sourced directly. SPO has become a critical discipline for precisely this reason—reducing unnecessary hops in the supply chain, consolidating SSP relationships, and prioritising paths that deliver efficiency without sacrificing quality.

- Budget fragmentation across platforms creates its own economic drag. When spend is distributed across five, seven, or ten platforms, each with minimum commitments, learning periods, and optimization cycles, the aggregate efficiency of the total media investment suffers. Consolidation promises simplicity, but it also introduces concentration risk and reduces competitive leverage.

When your media strategy is engineered around your KPIs instead of a platform's commercial incentives, the performance gap becomes undeniable. — Stephen Magli, CEO & Founder, AI Digital (AI Digital)

Platform consolidation vs ecosystem fragmentation

The tension between consolidation and fragmentation defines the strategic landscape for every marketer operating in the ad tech ecosystem structure.

Consolidation appeals because it reduces complexity. Fewer platforms mean fewer integrations, fewer reporting reconciliations, and fewer vendor relationships to manage. Large platforms actively encourage this logic. Google's Performance Max, Meta's Advantage+, and Amazon's demand-side tools all aim to absorb more of the campaign workflow into a single environment. The pitch is efficiency: let one platform handle targeting, creative, optimization, and measurement, and you simplify your operations.

The trade-off is control. Consolidation within a walled garden means accepting that platform's data policies, its attribution model, its optimization logic, and its inventory prioritisation. It means trusting that the platform's commercial incentives are aligned with yours—a trust that recent audit findings, supply-path investigations, and very public disagreements between holding companies and buying platforms have placed under sustained scrutiny.

Fragmentation, by contrast, preserves flexibility. Working across multiple platforms and partners allows advertisers to compare performance, negotiate pricing, access diverse inventory, and avoid dependence on any single vendor. The cost is complexity: more platforms to manage, more data to normalize, more operational overhead.

{{26-Digital-Advertising-Ecosystem-5="/tables"}}

The strategic question is not whether to consolidate or fragment, but where to draw the line for your specific business. The organizations that navigate this trade-off most effectively tend to share a common characteristic: they invest in a unifying layer—whether a technology platform, a managed service partner, or an internal capability—that sits above the individual platforms and provides cross-environment intelligence, governance, and control.

Why ecosystem governance is becoming critical

Governance is not a new concept, but its application to the digital advertising ecosystem is overdue. As the system has grown more complex, more expensive, and more opaque, the need for deliberate structures that define how platforms, partners, and data interact has moved from a best-practice recommendation to an operational necessity.

Governance in this context means establishing clear policies and processes for supply path management, so that every intermediary in the chain is there for a documented reason. It means defining measurement standards that apply consistently across platforms, even when those platforms resist interoperability. It means setting data handling protocols that comply with an expanding patchwork of state-level privacy laws—eight US states now enforce comprehensive consumer privacy legislation, with more expected in 2026.

Governance also means establishing accountability for how AI-driven optimization tools are deployed. As more buying decisions are delegated to machine learning models, the question of who reviews those decisions, against what criteria, and with what frequency becomes critical. AI that operates without oversight is not intelligent; it is autonomous in a system where autonomy and accountability are often in tension.

The organizations that treat governance as a strategic function—not a compliance checkbox—tend to achieve measurably better outcomes. The ANA's Q4 2025 benchmark confirmed that advertisers enforcing disciplined quality governance converted a significantly higher share of their programmatic spend into qualified impressions compared to their less disciplined peers.

💡 Related read: What is advertising governance in a fragmented ecosystem?

What marketers should do next

The digital advertising ecosystem is not going to simplify itself. Platforms will continue to build proprietary environments. New channels will emerge. Regulations will expand. The complexity marketers face today is a floor, not a ceiling.

Accepting that reality, the most productive response is not to wait for the ecosystem to consolidate around a simpler model, but to build internal capabilities and external partnerships that impose structure on the complexity.

- Audit your supply paths. Know how many SSPs carry your spend, which paths are direct, and where fees accumulate. The difference between a well-managed supply path and an unmanaged one can be measured in double-digit percentage points of wasted budget.

- Consolidate measurement before consolidating platforms. The priority is not fewer tools; it is a consistent framework for evaluating performance across the tools you use. Cross-platform measurement does not require a single platform. It requires a single standard.

- Invest in data interoperability. First-party data strategies only deliver value if the data can be activated, measured, and connected across environments. CDPs, clean rooms, and identity frameworks are investments in the connective tissue your ecosystem currently lacks.

- Evaluate AI with the same rigour you apply to any other vendor. Machine learning models are not neutral. They optimize toward the objectives they are given, within the constraints of the data they can access. Ensure your AI-driven tools are working toward your business outcomes, not a platform's default metrics.

- Seek partners that operate across the ecosystem, not within a single layer of it. The fragmented digital advertising landscape rewards specialists, but it punishes isolation. Partners that can provide cross-platform intelligence, supply-side and demand-side expertise, and transparent reporting across channels are better positioned to help you govern the ecosystem rather than simply participate in it.

The industry has fundamentally changed—the old way of buying media no longer reflects where consumers spend their time or how platforms actually operate. — Stephen Magli, CEO & Founder, AI Digital (AI Digital)

Conclusion: Control comes from understanding the system

The digital advertising ecosystem is not inherently inefficient. It becomes inefficient when it is not understood, not governed, and not managed with the same discipline that organizations apply to other complex operating environments.

The programmatic infrastructure that powers this ecosystem is extraordinarily capable. It enables reach, precision, and speed that manual processes could never deliver. But capability without governance produces waste. Scale without transparency produces opacity. Automation without oversight produces outcomes that serve the platform's objectives as readily as the advertiser's.

Competitive advantage in this environment does not come from choosing the right platform. It comes from structuring and governing the entire ecosystem—supply paths, data flows, measurement frameworks, partner relationships—so that every element works in service of the business outcome, not the intermediary's margin.

Global advertising spend surpassed $1 trillion for the first time in 2026. The organizations that capture a disproportionate share of value from that investment will be the ones that understand the system well enough to control it.

AI Digital operates at this intersection of complexity and control. Through its Open Garden framework, DSP-agnostic managed services, AI-powered supply selection, and Elevate intelligence platform, AI Digital provides advertisers and agencies with the cross-platform transparency, data-driven governance, and KPI-first optimization that the ecosystem demands. If you are rethinking how your media investment moves through this system, we would welcome the conversation.